The Ultimate Guide to Liquidation Part 2: Preparing for Liquidation

The terms ‘liquidation’ and ‘winding up’, just like the terms ‘bankruptcy’, ‘tax office’ and ‘new season of Married at First Sight’, carry a degree of anxiety. But they shouldn’t. Liquidation, or the ‘winding up’ of a company, can happen for many different reasons: it does not necessarily mean that the business is broken beyond repair.

- Introduction

- Unsecured creditor prospects in liquidation

- Options for creditors to rein in the costs of the liquidation

- Alternatives to liquidation for creditors

- The final verdict on the success rates of liquidation

- Prepare for a voluntary liquidation

- How do you choose the right liquidator?

- Why appoint a voluntary administrator at the 11th hour?

- Conclusion of Part 2

Introduction

This Ultimate Guide to Liquidation explains everything you need to know about liquidation and its alternatives in Australia. In Part 1, we considered the question ‘What is liquidation?’. We explained all the main types of liquidation in Australia (members’ voluntary liquidation, creditors’ voluntary liquidation and simplified liquidation). Briefly, we looked at some available alternatives (such as voluntary administration and debt restructuring).

In this part, Part 2, we look at how to prepare for liquidation. We begin by looking in greater depth at the shortcomings of liquidation (the returns for creditors are generally very low) before looking at general steps directors can take to prepare for liquidation, how to choose the right liquidator, and how the court will deal with attempts of directors to prevent winding up with the appointment of an 11th hour’ voluntary administrator.

In the next part, Part 3, we will look at how businesses can best deal with the aftermath of liquidation.

Unsecured creditor prospects in liquidation

In liquidation, the company is wound up, any remaining assets are realised and distributed to creditors. But who gets priority for the remaining assets? Priority for the proceeds of the winding-up goes to secured creditors. Even among secured creditors, some interests, such as a Purchase Money Security Interest (‘PMSI’) have ‘super-priority’ over other secured interests.

For unsecured creditors, creditors who do not have a registered security interest in the assets of the company, funds are distributed in order of priority as set out in section 556 of the Corporations Act 2001 (Cth):

- The costs and expense of the liquidation, including liquidators’ fees;

- Outstanding employee wages and superannuation;

- Outstanding employee leave of absence (including annual leave and long service leave);

- Employee retrenchment pay;

- Remaining unsecured creditors.

Given the order or priority, what are the prospects of the remaining unsecured creditors getting a return?

- In 2017, Australian Securities and Investments Commission (ASIC) data suggested returns to general creditors average 11 cents or less on the dollar in 96% of cases;

- In 2018, prospects of creditors reduced further with 97 per cent of cases resulting in returns of between zero and eleven cents.

These ASIC statistics are somewhat unhelpful because they include outliers (such as 100c returns) that distort the true average.

As such, these (miserable) statistics overstate the prospect of a return for the median creditor. Outcomes are skewed by a few larger businesses leaving more significant pay-outs. In our experience, the expected return for the median unsecured creditor is zero cents on the dollar. As the overwhelming majority of windings up end up in Australia are small-sized and family businesses with a small asset base, it is unsurprising that zero assets are leftover in so many cases.

However, it is not simply the state of the business itself that is resulting in such low returns. It is also clear that substantial liquidators remuneration and expenses are eating up the remaining assets in many cases. For a recent court decision that looked into the practice of excessive liquidator fees, consider Lock, in the matter of Cedenco JV Australia Pty Ltd (in liq) (No 2) [2019] FCA 93. In that case, the Federal Court objected to the liquidator’s rates as unreasonable (for example, $700 per hour for partners), when they were clearly out of step with market rates.

Our intention is not to demonise insolvency practitioners: they perform an important function to recycle business assets and oversee the integrity of this process. Their business model is risky because they are often committed to appointments where they might not be paid in full or at all (assetless companies). What can be criticised is the practice of target billing.

Target billing is where the insolvency practitioner loads up on billing in insolvency administrations that have assets, in order to compensate for assetless jobs. This practice is unfair to the creditors that miss out on dividends because of unreasonable fees.

It is also worth observing that the loss from over-the-top liquidator fees is not just a loss to individual creditors but constitutes a significant loss to taxpayers as well; the Australian Tax Office (ATO) is almost always the largest unsecured creditor and yet they have no priority and so are usually unable to recover unpaid taxes.

The Australian Small Business and Family Enterprise Ombudsman launched an inquiry into the effect of insolvency practices on small businesses and made a range of recommendations.

It is worth noting that the new simplified liquidation process (see Part 1) is intended to substantially reduce the cost of liquidation for small businesses by streamlining the liquidation process. Time will tell whether this improves the outcomes for unsecured creditors of those businesses.

Options for creditors to rein in the costs of the liquidation

In response to a perception that insolvency practitioner fees are too high and are having a negative impact on liquidation outcomes, a range of reforms were introduced in 2016, including enhanced powers for creditors to approve liquidator remuneration and expenses and the appointment of a ‘reviewing liquidator’. In the liquidation process, creditors need to consider:

- The remuneration and expenses approval process. In the case of a creditors’ voluntary liquidation (CVL), remuneration and fees must be approved by the creditors themselves, a committee of inspection, or the Court. If fees are not settled by either resolution of creditors or the committee of inspection then they must be set by the Federal or Supreme Court. To read more about the fee approval process see Part 3.

- Appointment of a Reviewing Liquidator. Creditors also have the option of appointing a ‘Reviewing Liquidator’ who is a registered liquidator appointed to review the remuneration and costs charged. There are two mechanisms for appointing a reviewing liquidator:

- by a resolution of creditors. If this occurs, the costs of appointing the reviewing liquidator are added to the costs of liquidation;

- without a resolution, but with the consent of the liquidator. If this occurs, the applicant creditor must bear the costs of appointing the reviewing liquidator.

This Reviewing Liquidator can only look into:

- remuneration approved in the prior six months; and

- costs or expenses incurred during the previous 12-month period.

We discuss the role of the Reviewing Liquidator process in detail in Part 3. It is worth noting that, as the cost of the Reviewing Liquidator is added to the costs of the liquidation, this can further reduce the pool of money available to unsecured creditors. If the liquidator doesn’t have sufficient funds then the creditors may be called upon to provide an indemnity.

Another option for creditors seeking to rein in excessive liquidator remuneration and expenses is to make a court application. Under section 447A of the Corporations Act 2001 (Cth), the court has broad powers to make orders as it sees fit in relation to liquidation. This application allows creditors, others with a financial interest and directors apply to the court for an order:

- For a determination in relation to any matter related to the liquidation;

- That an individual be replaced as the liquidator;

- For remuneration.

As always with court proceedings, this will be an expensive and time-consuming process. This is why creditors aren’t enthusiastic about Court application.

Alternatives to liquidation for creditors

Given the poor prognosis for unsecured creditors, what other options do they have available to them? We already mentioned in the first section of this article that creditors could consider issuing a statutory demand for payment in order to ‘scare’ the debtor company into payment.

Other possible options include:

- Voluntary Administration. This process that is usually initiated by the directors of the company, seeks to arrive at a ‘Deed of Company Arrangement’ (DOCA) by agreement of creditors that will provide them with a better outcome than proceeding directly to liquidation. Note, however, that the rates of return for this process are also dire for unsecured creditors. Through a DOCA, creditors receive, on average, 5-8 cents on the dollar. Here you can read more about the success rates of voluntary administration.

- Schemes of arrangement. These relatively uncommon arrangements, regulated under Pt 5.1 of the Corporations Act 2001 (Cth), are binding, court-approved agreements, allowing for the reorganisation of the rights and liabilities of members and creditors of a company. Note, however, that as this is a court-supervised process involving significant input from the ASIC, it is by no means a cheap or quick option. Note also that, this option is limited to big corporates.

- The new debt restructuring process for small businesses. This new process which comes into effect 1 January 2021 creates a new role of a ‘small business restructuring practitioner’ (‘practitioner’). This individual can be appointed by the directors of a struggling business to work out a restructuring plan and get it approved by creditors. We discuss this in detail in Part 1;

- Informal mechanisms. Another possibility is for creditors to consider negotiating directly with the company without putting them into liquidation. While, in some cases, creditors may appreciate the satisfaction in ‘punishing’ debtors through liquidation, the non-liquidation is likely to lead to a better financial outcome for the creditors. This is ruled out however when creditors don’t have sufficient trust in place.

The final verdict on the success rates of liquidation

All-in-all, forcing a liquidation is often not a cost-effective or efficient means for a creditor to get a return on what they are owed. There has been a significant rise in CVLs and a reduction in court-appointed liquidations in recent years. This, perhaps, recognises both the expense in creditors going through the court process, as well as a tendency for existing liquidation processes to benefit the debtor company and liquidators more than creditors. For example, it is likely that directors often use CVL process to avoid their own liability in many cases, such as personal liability for tax debts.

In light of this, it is worth non-director creditors exploring other options, besides liquidation, in order to get the best chance of a return on their debt. Often an informal negotiation process for repayment of the debt may be the best option for creditors. Otherwise, creditors may need to be realistic! Steer clear of bad payers and clients with poor credit to avoid liquidations. Credit insurance is another protection option.

Prepare for a voluntary liquidation

The terms ‘liquidation’ and ‘winding up’, just like the terms ‘bankruptcy’, ‘tax office’ and ‘new season of Married at First Sight’, carry a degree of anxiety. But they shouldn’t. Liquidation, or the ‘winding up’ of a company, can happen for many different reasons: it does not necessarily mean that the business is broken beyond repair. Liquidation has a different impact on a company depending on how, and why, it was initiated. Matters to consider include:

- Has a winding up petition been filed in court with respect to the company? If so, depending on whether you can fight the petition in court, the company may be wound up and liquidated, whether you like it or not. This is an ‘involuntary’ or ‘compulsory’ liquidation;

- Is the company financially healthy, but no longer fit-for-purpose, or superfluous for some reason? In this case you may be able to consider a members’ voluntary liquidation (‘MVL’);

- Is the company insolvent, or likely to become insolvent? A company is insolvent when it is unable to pay its debts as they fall due and payable. At this point, voluntary administration, or CVL become possible options.

Let’s consider this third option in greater detail. In voluntary administration, an independent professional is handed the reins by the directors, in an attempt to negotiate a DOCA for the payment of creditors. In a CVL, a liquidator is appointed in order to terminate a company and realise its remaining assets for the benefit of creditors.

The appointment of either the voluntary administrator or liquidator also has the effect of stopping all action for debt recovery from creditors. It is worth noting that while liquidation does end the life of a particular company, it doesn’t necessarily mean the end of the ‘business’, broadly conceived. When a voluntary liquidation is deployed as an element of a pre-pack insolvency arrangement (‘pre-pack’), the substance of the business can survive in another form. We discuss this possibility in more detail below.

When might voluntary liquidation be a good idea?

If your business is insolvent, or likely to become insolvent, you need to take immediate action. If you don’t take some kind of action, you may be in breach of your duty as a director to prevent insolvent trading of the company (see section 588G of the Corporations Act 2001 (Cth)). What are the possible actions you might take?

- You could sell business assets to third parties to pay down debt;

- You could appoint a voluntary administrator;

- You could consider a formal debt restructuring by a ‘practitioner’ (where an eligible small business);

- You might consider an informal ‘work around’, such as securing rescue finance, an extension of terms from suppliers, or a payment plan with creditors, in order to bring the company definitively back into solvency;

- You might consider informal restructuring via a pre-pack. In a pre-pack, the assets of the existing company are sold for appropriate consideration to a new company (which may have the same directors as the old company). The old company is then liquidated. The transaction might be completed before or after appointment of the liquidator, depending on the circumstances of the case.

For more information on pre-packs, see What you need to know before you pre-pack (to avoid phoenix activity).

There may be situations where none of the above possibilities are appropriate. For example, where there is no longer a valuable business proposition underlying the business at all. In that case, it may make sense for directors to appoint a liquidator immediately.

It may also be sensible to appoint a liquidator where creditors are about to pursue the winding up of the company via a compulsory liquidation. This way, directors can retain some control over the appointment process.

Note also that temporary COVID-19 reforms mean that there is reduced urgency to rush into liquidation or voluntary administration. These reforms mean that:

- It is much more difficult for a creditor to pursue a compulsory liquidation, as the criteria for statutory demands for payment of debt (‘statutory demand’), which are commonly employed as evidence of insolvency, have changed. The minimum amount required for a statutory demand has increased from $2,000 to $20,000, and the time for payment has extended from 21 days to 6 months;

- Directors have an additional ‘safe harbour’ from insolvent trading, where loans are acquired in the ordinary course of business. A ‘safe harbour’ means that the director of the company is not liable for allowing insolvent trading under the Corporations Act 2001 (Cth) while pursuing the permitted business rescue activity.

You can read more about this at Is your business insolvent because of COVID-19? What to do next (for SMEs).

While the temporary COVID-19 measures end on 31 December 2020, it is worth noting that the new restructuring process will also reduce the urgency of liquidation for small businesses. A ‘safe harbour’ will apply to all eligible businesses that have initiated the restructuring process. Read more about this process in Part 1.

How are directors going to know if a voluntary liquidation is the right move? Below we set out the steps that should be taken in working this out.

Prepare for a voluntary liquidation: preliminary assessment of the books

As we discussed in our complete guide to voluntary administration, the first step is to get the books in order to get a clear picture of your financial situation. This will determine whether formal insolvency options should be pursued, or whether you still have informal options open to you.

When looking at your financials, you need to consider:

- Your bookkeeping systems. Without having an accurate and up-to-date record of your revenue, expenses, assets and liabilities, you will have little idea whether your company is solvent or insolvent;

- Your cash position. Look at your current ratio (current assets/current liabilities), quick ratio (liquid current assets/current liabilities) and operating cash flow ratio (operating cashflow/current liabilities), to determine whether you have the requisite cash coming into keep paying your bills;

- The state of your accounts payable. Note, in particular, whether any statutory demands for payment of debt have been made, and whether you can cover your upcoming tax liability;

- Reviewing asset structuring. Does the company in difficulty actually own the relevant assets (or are they leased from another entity, for example)? This means you can assess which assets would need to be liquidated if a liquidator is appointed;

- The state of the directors’ loan accounts. It is common for directors of SMEs to draw down on the business through a loan account, rather than be paid entirely through a salary. There is the potential for this loan to be called in, when a liquidator is appointed, so you need to work out what your position is here.

Prepare for a voluntary liquidation: solvency review

Once you have informally assessed your finances, you need to get a professional to conduct a solvency review. This is crucial, because if the company is solvent, then this has an impact on which options are available to directors to save the business. Directors of a solvent company can initiate an MVL rather than a CVL. The advantage of this option is:

- It is likely to be cheaper, as there is no need to appoint a registered liquidator;

- Members (i.e. shareholders) get to control the direction of the liquidation;

- The liquidator need not be independent of the company;

If, after a solvency review, the company is determined to be insolvent, an MVL will not be an option. At this point, you need to consider other options, including:

- Voluntary administration. Like the appointment of a liquidator, the appointment of a voluntary administrator will halt any claims against the company, while the voluntary administrator attempts to negotiate a ‘deed of company arrangement’ with the creditors. Unfortunately, the rate of success of voluntary administration, particularly for SMEs, appears to be abysmal. For more information see our article on voluntary administration;

- Use the ‘safe harbour’ under section 588GA of the Corporations Act 2001 (Cth), to enable an informal workaround to insolvency. This could include negotiating more favourable payment terms with creditors or accessing rescue finance;

- If eligible, initiate the new debt restructuring process for small businesses;

- Use the safe harbour to restructure using a pre-pack. This will also result in the liquidation of the original company (though, done correctly, the substance of the business will continue);

- Immediately initiate a CVL. This will mean a halt to all creditor proceedings against the company. However, this will also mean the end of the business as a going concern.

- Hire an insolvency expert to see if you can develop a bespoke hybrid solution (call Sewell & Kettle Lawyers)

Prepare for a voluntary liquidation: assessing your liability before appointment of the liquidator

An important consequence of a liquidator being appointed is that the liquidator is empowered to investigate the affairs of the company. This means that they can question, and potentially take action, with respect to prior actions of directors. Directors need to consider the possibility of:

- Uncommercial transactions. Transactions are deemed uncommercial if it is deemed that a reasonable person, considering the benefits and detriments of a given transaction, would not have entered into it. An uncommercial transaction can only occur where insolvency can be proven at the time of the transaction;

- Unfair preference claims. These happen where a creditor is paid for something that they are owed, which gave them an advantage over other creditors, where that creditor knew or ought to have known the company was insolvent;

- Unreasonable director-related transactions. These transactions are ones where directors enter into transactions that a reasonable person in the director’s circumstances would not have;

- Creditor defeating dispositions. These transactions are commonly referred to as ‘illegal phoenix activity’. They occur where there is a “disposition of company property for less than its market value (or the best price reasonably obtainable) that has the effect of preventing, hindering or significantly delaying the property becoming available to meet the demands of the company’s creditors in winding-up.”

In general, directors need to take a strategic approach to the payment of their debts before the CVL commences. In particular, they should look at whether any debts which have director personal guarantees attached can be paid. Note however that in doing so, legal advice must be sought to ensure that legal liability is not incurred for any of the matters set out above. Restructuring an insolvent business with asset transfers requires receiving an expert professional opinion to ensure that none of the above illegal or voidable transactions are undertaken.

Director action during and after a voluntary liquidation

Once the liquidator is appointed, directors are obligated to support the conduct of the CVL in various ways. This includes:

- advising the liquidator on the location of company property;

- providing books and records;

- providing a written report about the company’s affairs within five business days;

- meeting with the liquidator to help with their inquiries, as reasonably required;

- if requested, attending a creditors’ meeting to provide any required information.

The CVL will come to an end once the liquidator has realised and distributed the company’s remaining assets and lodged a final account with the ASIC.

Three months after this point, the company will be automatically de-registered.

Key takeaways when preparing for voluntary liquidation

When preparing for liquidation, company directors should consider the following factors:

- Liquidation comes in many forms. Not all liquidations imply something has gone wrong in a company;

- Before considering appointing a liquidator, directors need to take stock of their financial situation. This means basic bookkeeping, looking at key financial ratios and assessing the state of creditors;

- The next step is getting a professional opinion on the solvency of the company. This will determine which type of liquidation is available (MVL, CVL or simplified liquidation);

- Once it has been determined that a liquidator should be appointed, directors need advice in order to carefully assess their legal liability;

- Once a CVL is underway, directors need to support the liquidator in various ways as required by law.

How do you choose the right liquidator?

The company liquidation process (a CVL for insolvent companies) can be a long and winding road for company directors. While directors might get to appoint the liquidator, they don’t owe the directors or owners any legal duties, so it is best to pick an ethical and commercially-minded liquidator. If you pick a “salesman” liquidator you may find that they’ll try to “supersize” your liquidation. The size and culture of the liquidator’s firm should be carefully considered because you will likely be dealing with them a lot. It is also important for directors to realise that the process of appointing a liquidator usually stinks, as there is often a lack of transparency and many conflicts of interest.

Why does it matter to pick the right liquidator?

- Although directors may appoint the liquidator in a creditor’s voluntary liquidation, the liquidator has the legal duty to act for the creditors;

- While the liquidation is running, the directors will be subject to investigations by the liquidator and they may be sued to recover funds or as punishment for breaching their duties to the company;

- The liquidator may communicate with the media about the liquidation and the director’s conduct;

- The liquidator has a legal duty to report impropriety to ASIC and/or the police;

- It is highly unlikely that the liquidator can be removed by the directors – so selecting a liquidator is a decision that is probably irreversible.

Take-away for directors: Overall, a company liquidation is stressful – so why pick someone unless they’re the best person for the job?

When do you appoint a liquidator?

When a company is insolvent and the directors decide to cease trading, a voluntary liquidator should be appointed.

If the directors put off appointing a liquidator for too long, they may increase their risk of facing the following consequences:

- A director’s penalty notice being issued by the ATO to pierce the corporate veil (read our blog post about DPNs – Director Penalty Notices for further information);

- Creditors taking action to wind up the company themselves and appointing their preferred liquidator: Read our blog post about applications to wind up a company in insolvency;

- An action against the directors for breaching their legal duties by trading whilst insolvent

The process of choosing a liquidator usually stinks

Corporate liquidations can be highly profitable jobs for an insolvency practitioner. The partner hourly rates of liquidators are usually in the order of $750 (or more) and that’s before you consider the leverage model that results in billings from the multiple levels of accountants and administration staff working on the appointment. This means that it is a very attractive proposition for a liquidator to take an appointment where assets remain in the company (or at least claw-back claims) when they are appointed.

If a company director doesn’t already know a company liquidator, it is likely they will be introduced by a trusted adviser such as their accountant or solicitor. The result of this is that the insolvency market is completely driven by referrals and a sophisticated array of models for incentivising referrers. For small firm accountants, the incentive is likely to be cheap for the liquidator, and they may receive an invitation to the football or the races. Lawyers could receive lucrative legal work from a liquidator, but it is illegal for lawyers to receive cash payments. There are also armies of referrers that charge liquidators direct cash commissions for appointments and provide consulting services for directors.

Phoenix operators are also referrers to liquidators and their preferred model is to seek low cost liquidations with full knowledge that the liquidator will look to take legal action against their director clients. For more information on phoenix activity, read our article and watch an interview with our Principal, Ben Sewell: The Complete Guide to Illegal Phoenix Activity

Company directors should realise that company liquidation is an extremely competitive market and that virtually any liquidator could take their appointment. This means that they have the responsibility to carefully assess who they appoint in advance. If company directors get stuck with a liquidator that their accountant is “mates” with, the director may be inadvertently facilitating secret commissions and signing themselves up for a suboptimal appointment.

Take-away for directors: Understand that the process for referrals in the insolvency industry generally stinks and keep an eye out in case your professional adviser is preferring their own interests to yours.

Consideration 1: The size of the firm is important

The first consideration for choosing a liquidator is to work out the optimal firm size for the type of appointment.

What type of liquidator firms are there?

- Large-sized firms: firms with greater than 20 partners, big city offices and sophisticated support services

- Medium-sized firms: firms with more than 5 partners, large offices and limited support services

- Small firms and sole practitioners: firms with 1-3 partners, a single office and no support services

What are the capabilities of liquidator firms?

- Large-sized firms: Undertaking large liquidations for companies with more than 200 employees with IT and forensic accounting support

- Medium-sized firm: Undertaking small and medium-sized appointments (companies with less than 200 employees) but without sophisticated IT and forensic accounting support

- Small firms and sole practitioners: Largely undertaking small business liquidations (less than 20 employees) but without the capability to deal with IT issues or forensic accounting issues

What are the ideal referrers for liquidator firms?

- Large-sized firms: Banks and private equity funds

- Medium-sized firms: Large accounting firms and large law firms

- Small firms and sole practitioners: Small accounting firms, small law firms and consultants

If you are a director of a large company (more than 200 employees) then you’ll probably need a large-sized firm for the simple reason that nothing will get done otherwise. For example, the task of organising a creditors’ meeting for creditors across Australia and overseas may mean that a firm without this capability will get stuck at the first hurdle and upset all of the creditors. The last thing that you want is for the body of creditors in a large liquidation to have any concerns that the liquidation isn’t being professionally run.

The key limitation is usually economic because the larger a liquidator’s firm is, the more expensive it will be to engage them. However, in larger liquidations, a larger firm may be necessary to get a better quality administration process and a faster result. In any liquidation, it is likely that the directors want the business closed down and to have their record of conduct given a “tick” by an investigating liquidator. Further, if the key creditor is a bank or large financier, they may require the appointment of a liquidator who is on their panel.

The key downside of a smaller liquidation firm is that they will be slower in achieving their deliverables. However, they will be a lot cheaper. If a company liquidation has less than $200,000 in assets then directors should look to a smaller firm or sole practitioner as being fit for purpose.

Take-away for directors: Appoint a firm that is the right size for the work that needs to be done in your liquidation.

Consideration 2: The culture of the firm

Organisational psychologists will tell us that culture is “hard-wired” into an organisation. This means that you can’t expect any organisation to change its values or methodology because you ask them to. Culture is something that permeates “top-down” in an organisation, so the partners will give you the strongest indication of the firm’s overall culture. You’ll also need to work out ways to test the culture of the firm. Some ways to test their culture and values could include asking yourself:

- Do they offer you water in the board room?

- Do they show an interest in you?

- Do they contribute to society, e.g. by supporting a charity or through other CSR schemes?

- Are family values important to them?

What company directors want to avoid is becoming captive to an unethical and rapacious firm that only values the income they will receive. That firm won’t only be impossible to deal with, but they will also look for ways to improperly maximise their fee income. There are plenty of examples of overcharging and suspicious conduct of liquidators that can be found on the blog Sydney Insolvency News.

Take-away for directors: Appoint a firm that has appropriate values.

Consideration 3: Price

Like in any business transaction, the price of the services on offer is a critical consideration. If possible, company directors may try to persuade a liquidator to take the appointment on the basis that they get paid from the liquidation of the assets in the company itself. If the company is assetless, then they may be asked for advance payments, or to promise to indemnify the liquidator for a sum between $5,000-$100,000.

The proposition that a liquidator will take on an appointment for a fixed fee is wrong and also misleading. It is misleading because no matter what is promised in advance the liquidators can later seek approval from creditors for a fee adjustment. Company directors need to keep in mind that liquidators don’t create profitable businesses through the number of $10,000 jobs they do, but through the jobs that generate fees in excess of $100,000.

Take-away for directors: See if you can find a liquidator that will take the appointment with no upfront fee.

Consideration 4: Experience is paramount

There are some insolvency firms that are staffed by a young and vibrant group of accountants. These are precisely the liquidation firms that any sensible company director should avoid. This is because they are focused on leverage through billing, but they have insufficient experience to accomplish difficult tasks. This can be frustrating for directors because they may want to meet with their appointee but instead, they are serviced by a young accountant with no strategic vision or tactical understanding of what needs to be done. How could a 25 year old accountant possibly understand a company liquidation?

Experience is essential for any team that supports a liquidator because the actual appointee’s time is limited. Their team can only gain confidence and skill through working on liquidations similar to your own. The same applies to the liquidator who is specifically appointed to your matter.

Take-away for directors: Only appoint experienced liquidators with good teams.

Consideration 5: Ethical and hard working

One type of liquidator to avoid is the “salesman” liquidator. This liquidator will spend more time lunching and drinking with referrers than doing actual work! They’ll probably be likeable and engaging, but they won’t be able to demonstrate a track record that you are comfortable with. Like a used car salesman this archetype will work hard to get the “sale” over the line and then pass you on to other members of their firm to do the actual work.

At one time it was accepted that successful liquidators would do only a couple of days of actual work a week and then spend the rest of their time cultivating referrers at long lunches and drinks functions. This writer’s opinion is that there is plenty of empirical evidence to support the proposition that there is a correlation between unethical conduct and drug and/or alcohol addictions.

Company directors should only engage hard working and ethical liquidators. This type of liquidator is the most likely to be able to negotiate successfully through the difficult liquidation process.

Take-away for directors: Engage only ethical and hardworking liquidators because they are more likely to follow through.

Consideration 6: Commercially minded

Liquidators need to make commercial decisions quickly.

The types of commercial decisions that liquidators need to make include:

- Determining the process for selling assets and the best price that can be obtained for those assets

- Whether to commence proceedings against creditors to recover unfair preference claims

- Whether it is feasible to commence insolvent trading actions or undertake any other claw-back actions against the directors

- Whether to reverse any pre-appointment transactions that the directors entered into (i.e. phoenix activity)

- How long to continue a liquidation and whether to initiate extensive investigations into the director’s conduct through examination hearings in open court

Directors have no interest in engaging an intransigent liquidator who undertakes actions that only have the benefit of increasing their chargeable hours without any tangible benefit for creditors or other stakeholders.

The cost of not engaging a commercially minded liquidator is that you may be caught up in the quests, meandering explorations, pet hates, arguments with the ATO and bitterness that is sometimes associated with those liquidators that aren’t commercially-minded.

Take-away for directors: Engage a commercially-minded liquidator.

Who to avoid: The incompetent liquidator

This commentary should also be read as including incompetent staff. The first negative indicator of incompetence is usually that the liquidator and their staff aren’t members of the CPA or CA professional accounting associations.

Sometimes directors think it is a good idea to appoint the most incompetent liquidator they can find. Usually this liquidator has failed in a larger firm and then decided to grind out a living at a small or medium-sized firm. The logic is that by appointing an incompetent liquidator they will avoid a thorough investigation that may turn up phoenix activity or antecedent transactions that can be clawed back. One example of this is when the director’s accountant “journals out” a director’s loan account as a method of helping the directors avoid being sued for a common debt claim.

The logic of appointing an incompetent liquidator is often persuasive for an 11th hour appointment but over time, the directors are guaranteed to be frustrated by this approach. The issue is that given the complexity and conflict that can arise in a liquidation, the last thing a director needs is a protracted liquidation with someone who frustrates all stakeholders. One example is where a liquidator tells a director that they have “never” sued anyone for insolvent trading. This may be true but the director can assume that the novelty will be attractive if they can put a claim together against their appointing director.

The reality is that liquidators very rarely sue directors for insolvent trading anyway, regardless of whether the liquidator is competent or not.

Take-away for directors: Avoid a liquidator who is obviously incompetent.

Who to avoid: The corrupt liquidator

There is a long history of corrupt insolvency practitioners who take kickbacks in exchange for ignoring director misfeasance. There is also a long history of insolvency practitioners who illegally benefited from appointments by taking money or benefits from a company liquidation. The liquidator is in a trusted position and other than relatively rare audits by ASIC, they are largely left to their own devices for company liquidations.

It is going to be virtually impossible to identify these corrupt insolvency practitioners from outward indicators. One negative indicator would be that they imply in conversation with a director that they will ignore a legitimate claim against a director such as a director’s loan account or an uncommercial transaction. They would also be obviously corrupt if they asked for a cash payment that would be kept “off the books” and therefore corruptly procured by the liquidator.

The logic behind appointing a corrupt liquidator may be that the directors believe it to be the only means of avoiding personal liability for insolvent trading or uncommercial transactions.

Directors in Australia are generally protected by the ‘corporate veil’ so they are very unlikely to be sued by liquidators. There is also a safe harbour from insolvent trading so directors can attempt an informal restructure process if their company is insolvent. This means that directors can now legitimately attempt informal restructures in Australia before being forced into liquidation or voluntary administration. By the time the directors appoint a liquidator, they will have exhausted all other options or it will be after a pre-pack insolvency arrangement is completed.

The downside of a crooked liquidator is that they are just as likely to turn on the directors as they are to adhere to their pre-appointment promise to “look the other away”. A good example of this is the case of Pino Fiorentino (read ASIC press release 14-160MR). Mr Fiorentino was struck off after he was found to have failed to properly investigate phoenix transactions. An interesting finding from the investigation was that despite not investigating the phoenix activity, the liquidator sued his directors anyway.

Another example of a corrupt liquidator is the case of Stuart Ariff who was a liquidator convicted of fraud. He used funds from a company in liquidation for limousines, an international holiday at a luxury resort for his family, hairdressing bills, bottles of wine, computers, rent payments, and tickets to the State of Origin and NRL Grand Final.

Senator John Williams (aka Wacka), a warrior for insolvency reform expressed frustration about the insolvency industry and the lack of movement on complaints about liquidators by ASIC:

“Senator John Williams said that… each week, at least one complaint was made to his office about a dodgy liquidator. ‘Most of the complaints include details and proof of wrongdoings, but where’s ASIC? What’s it doing to clean up this industry?’ he said.”

[Source: AFR article 20 December 2011, Rome burns, ASIC shows bankrupt determination, by Adele Ferguson]

Take-away for directors: Don’t put your liquidation in the hands of a crooked liquidator because you’ll be stuck with them.

Who to avoid: Referral services

There are numerous online referral services that promise to manage the insolvency process and provide consulting services. If the sole service they deliver is to assist directors in appointing a liquidator, it is likely that they will add no real value and only increase the overall price of the services. There are plenty of liquidators in the market that will offer low cost or speculative appointments (if the company holds saleable assets) rendering the assistance of referral services superfluous.

If the service that is being sought is advice about risk to directors, then consulting a lawyer and the insolvency practitioner themselves would be a sensible first step.

There are also phoenix operators that offer to assist directors to defraud the ATO and then find compliant liquidators afterwards. The reality is that they appoint underfunded liquidators and dispose of the books and records that could assist the liquidator in conducting investigations. This is usually short-sighted and liquidators can now access assetless administration funding from ASIC to investigate the directors.

Take-away for directors: Don’t use a referral service because it will only add to the overall price without adding value.

How do you test whether you’ve picked the right liquidator?

If you’re satisfied that you have found an experienced, ethical, hardworking and appropriate liquidator you should conduct the following tests:

- Ask them to provide references from other directors of liquidated companies

- Ask them for case studies of companies like yours that they have liquidated

- Go through an experienced insolvency lawyer to test that they are genuine

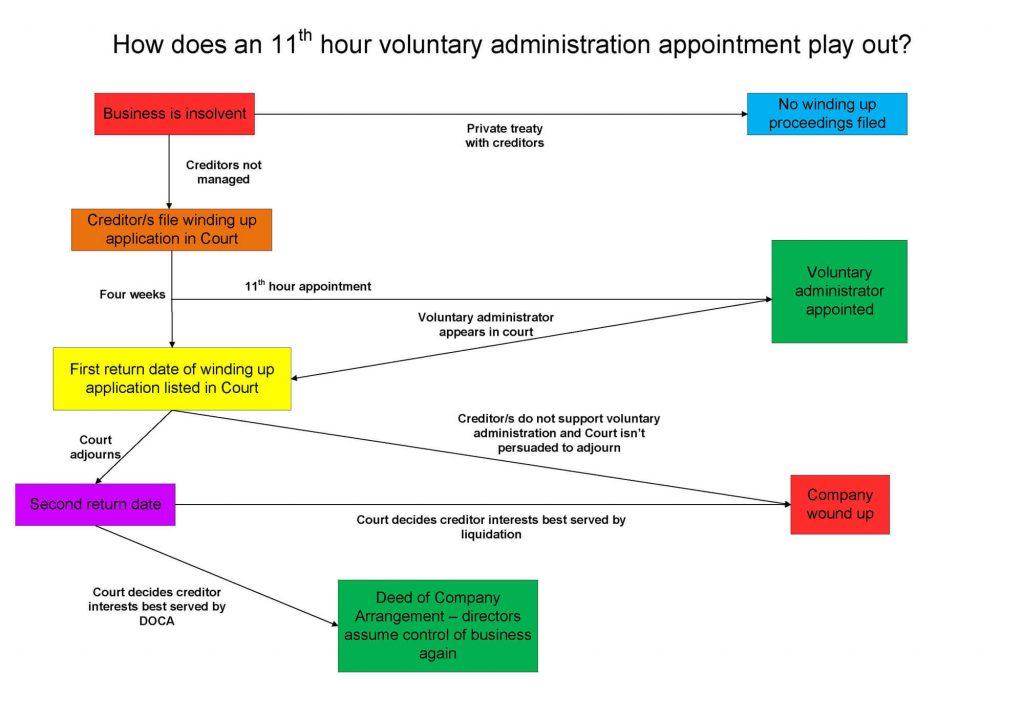

- Will a Court appoint a liquidator over the top of an 11th hour voluntary administrator?

Company directors are sometimes persuaded to appoint voluntary administrators while there is a winding up petition before the Court to liquidate the company. In this situation, the voluntary administrator/s will need to appear in Court and convince the Judge it is in the best interests of creditors to allow the voluntary administration to continue (rather than immediately winding up).

The key issue for directors is that it is not a relevant consideration for a Court to value saving owner’s equity (they have an uphill battle because the Court will be sceptical).

We explain the process involved below. We look at:

- Why would directors appoint a voluntary administrator at the 11th hour?

- How does court liquidation occur?

- The test set out in section section 440A(2) of the Corporations Act 2001 (Cth)

- Relevant case law: Weriton Finance Pty Ltd v PNR Pty Ltd [2012] NSWSC 1402, Re Laguna Australia Airport Pty Ltd [2013] FCA 1271, Re Offshore & Ocean Engineering Pty Ltd [2012] NSWSC 1296, Lubavitch Mazal Pty Ltd v Yeshiva Properties No 1 Pty Ltd (2003) 47 ACSR 197, Deputy Commissioner of Taxation v QBridge Pty Ltd [2008] FCA 1300.

Overall, it matters less when and in what circumstances the voluntary administrator was appointed, and more whether the creditors are better served by the administration or by a liquidation; this is what will affect the judge’s decision to grant a winding up application.

Why appoint a voluntary administrator?

The appointment of a voluntary administrator is usually initiated by the director seeking to save their company. It provides a moratorium from creditor action which allows the company to restructure without creditor interference (other than via a winding up application). The optional outcome for directors is a compromise through a DOCA that reduces the company’s debts. If the voluntary administration leads to a successful outcome through the DOCA, the directors will be given back their powers and allowed time to try and bring the company back to long term profitability and sustainability.

Why appoint a voluntary administrator at the 11th hour?

The ’11th hour’ for a company is the time immediately before a Court date is listed for a compulsory winding up. The creditors (such as the ATO) have lost patience with directors and believe their interests are best protected by winding up, rather than waiting for the directors to straighten things out through a voluntary administration. This is a scenario where the creditors oppose an adjournment of the winding up process.

Appointing a voluntary administrator at the 11th hour is more than likely a last-ditch attempt by directors to delay a liquidation which would result in the death of their business. While a liquidation spells the end of a company, a successful DOCA arising from a voluntary administration will allow directors to return to trade.

How does court liquidation occur?

An application for an order to wind up a company can be taken to court (Federal or Supreme) to be heard by a Judge or Registrar. If the application is granted, the order for liquidation will be made and the Court will appoint a liquidator selected by the applicant creditor.

To find out more about creditor initiated winding up, read our articles:

- Applications to wind up a company in insolvency

- What are the grounds to set aside a statutory demand?

The legislation guiding a court’s decision

The legislation that a Court will use to decide whether to wind up is set out in the Corporations Act 2001 (Cth). Section 440A(2) of the Corporations Act 2001 (Cth) provides that a Court must adjourn a hearing of an application for an order to wind up a company where that company is under administration, and the court is satisfied that it is in the interests of the company’s creditors for the company to continue with administration rather than be wound up.

This means that wherever there is an application to wind up a company (i.e. have it put in liquidation) and the company is currently undergoing voluntary administration, the Court must decide whether voluntary administration or liquidation would better serve the interests of the creditors – not the directors, or the business itself – in determining whether to wind up immediately.

The consequence of this legislation is that in any application for an order to wind up a company if the application is made by or on behalf of creditors who are primarily in support of the order, the directors and administrators must convince the Court that it is actually in the interests of the creditors that the company not be wound up.

Application in case law

Recent case law applying s 440A of the Corporations Act 2001 (Cth) has supported a common-sense interpretation of the section in the following ways:

- For the Court to be required to grant an adjournment, it must be satisfied that it is in the creditors’ interests to continue the administration in all the circumstances, which involves there being a sufficient possibility – as distinct from mere optimistic speculation – that creditors’ interests will be accommodated to a greater degree in an administration than in a winding up (Weriton Finance Pty Ltd v PNR Pty Ltd [2012] NSWSC 1402 at [16]-[21])

- The defendant company (i.e. the voluntary administrator’s lawyers) bears the legal burden of satisfying the Court that an adjournment should be granted (Re Laguna Australia Airport Pty Ltd [2013] FCA 1271 at [11])

- A substantial degree of persuasion that administration rather than liquidation is in the best interests of the company’s creditors is necessary. This means proof is actually required (Re Offshore & Ocean Engineering Pty Ltd [2012] NSWSC 1296 at [6])

And, most relevantly:

- The Court will view with scepticism the appointment of administrators at the last minute in the face of winding up proceedings (Re Offshore & Ocean Engineering Pty Ltd (supra) at [16])

In weighing the issue of how and who can determine whether administration or liquidation best serves the interests of creditors:

- Particularly in the case where commercial judgments may differ, there is force in the view that creditors are the best judges of their own best interests… But while I regard the opinion of an insolvency practitioner in this respect as relevant, ultimately it is for the judgment of the Court whether the continuation of the administration, as opposed to an immediate winding up, is in the interests of creditors. (Re Offshore & Ocean Engineering Pty Ltd)

- It may be said, why should this decision not be left to the creditors?… the overwhelming majority of whom have indicated a disposition in favour of adjourning the application to permit them to consider the DOCA. However, they have not been presented… with the fundamental truth… Ultimately the Court has to be satisfied that it is in the best interests of creditors. (Re Offshore & Ocean Engineering Pty Ltd)

In summary:

- For an application to be rejected, there must be a sufficient possibility that administration will accommodate the creditor’s interest to a greater degree than liquidation

- The defendant company (being the directors and administrators) bears the burden of proof for establishing why an application should be granted

- There must be substantially persuasive evidence that administration would be better than liquidation for the administration to be allowed to continue

- The Court will likely look at an 11th hour appointment of a voluntary administrator as a negative reflection on the efficacy and value of administration over liquidation

- Ultimately, while the opinions of creditors and insolvency practitioners will be considered, the determination of what is in the creditors ‘best interests’ and how those interests will best be served is left to the discretion of the judge

Further examples

- Lubavitch Mazal Pty Ltd v Yeshiva Properties No 1 Pty Ltd (2003) 47 ACSR 197

This case concerned an application for an adjournment of proceedings to wind up a company which had (very recently) been put into voluntary administration. The judge allowed the application in part, deciding that the appointment of the provisional liquidator would be preferable to salvage as much of the company as possible (and more could be salvaged through liquidation than through voluntary administration).

“On the evidence there was no prospect that a proposal might emerge for a deed of company arrangement that would produce a larger or accelerated dividend for the creditors than in a winding up. The evidence to the contrary was no more than optimistic speculation. For the same reasons CA s 440A(3) did not preclude the appointment of a provisional liquidator.”

“Section 440D of the Corporations Act 2001 (Cth) states that during the administration of a company, a proceeding against the company cannot be begun or proceeded with except with the administrator’s written consent, or the leave of the court.”

This case shows that provisional liquidators can and will be appointed by the court over the top of an 11th hour voluntary administrator.

- Deputy Commissioner of Taxation v QBridge Pty Ltd [2008] FCA 1300

This case concerned winding up proceedings before the court. Immediately prior to the commencement proceedings (at quite literally the 11th hour), voluntary administrators were appointed. Here, Greenwood J held the following:

“Accordingly, what I propose to do is this. I will grant the adjournment of the application for the winding up order for, in effect, a period of eight days by which time the voluntary administrators will have had an opportunity to determine whether the amount of $100,000 is paid tomorrow and, secondly, whether, based upon their expertise and experience generally, the responses that they obtain from St George and/or Downer EDI leads them to believe that there is any prospect of a Deed of Company Arrangement emerging which would result in a dividend to creditors greater than a dividend upon liquidation or whether there is a prospect of a sale of the business either at an amount which would discharge the creditors in total as is suggested or at some lesser amount which would result in a calculation of a dividend which might be favourably compared with that obtained in a liquidation.”

This decision shows that while the court is, in favourable circumstances, willing to maintain last minute voluntary administration appointments, they will still be treated with a degree of scepticism, and (as was the case here) liquidation will not be entirely ruled out, but rather put aside for a second return date.

Key takeaways

- Voluntary administration will always lead to either a deed of company arrangement or a liquidation anyway

- Australia exhibits a general culture of intolerance and judgment towards the process of voluntary administration, and as a result, goodwill value and reputation are often lost, contributing to poor rates of success

- It is not the priority of the Court to ‘save’ a business (only to protect creditors)

- Courts will likely make a prima facie judgment (or a ‘smell’ test) of whether the voluntary administration seems beneficial or not very quickly

- Overall, it matters less when and in what circumstances the voluntary administrator was appointed, and more whether the creditors are better served by the administration or by a liquidation; this is what will affect the judge’s decision to grant a winding up application.

Conclusion of Part 2

If considering liquidation, the first important factor to note is that the return for unsecured creditors is usually very small. In nearly all cases, 10 cents on the dollar or less is expected. It is possible that the new simplified liquidation process could result in better returns for the creditors of small businesses, however.

Once directors think that insolvency is a possibility, they need to prepare for the possibility of liquidation and other formal insolvency processes. We set out the steps directors need to take in assessing their books and evaluating their liability before initiating a formal insolvency process.

Once the decision to go into liquidation has been made, directors need to ensure they choose the right liquidator. We set out key factors in making this decision including the size of the liquidator firm, their culture, price, experience and ethics.

Finally, we considered the possibility of directors appointing a ‘11th hour’ voluntary administrator to prevent imminent liquidation. Both the Corporations Act 2001 (Cth) and significant case law confirm that the courts will only allow this to occur where an applicant can prove it will be in the best interests of creditors (not directors, or the business itself).

In the next and final part of this Ultimate Guide to Liquidation, Part 3, we will consider how directors and creditors can respond to liquidation. This includes setting out how liquidators can be replaced, how their conduct can be reviewed, and how businesses can best manage the fallout of a liquidation.