Ultimate Guide to Liquidation Part 1: What is Liquidation?

It has been evident for a long time that Australia’s ‘one-size-fits-all’ liquidation model is inappropriate for SMEs. This inadequacy has become particularly evident in the wake of the COVID-19 related economic turbulence.

- Introduction

- What is liquidation or winding up?

- Voluntary liquidation and insolvency

- The key elements of a members’ voluntary liquidation (MVL)

- The key elements of a creditors’ voluntary liquidation (CVL)

- How MVLs and CVLs compare to other insolvency processes

- The new formal debt restructuring process

- The new simplified liquidation process for small businesses

- Avoiding formal insolvency appointments

- When you shouldn’t appoint a voluntary liquidator – a checklist

- What is the creditor power to request information from liquidators?

- What is the Fair Entitlements Guarantee (FEG) scheme?

- Voluntary liquidators no longer required to hold first meetings

- Conclusion of part one

Introduction

The liquidation or winding up of a company is the final step in ‘ending’ the life of a company. It refers to the final stage of realising a company’s remaining assets and distributing them to creditors, according to a set hierarchy of ‘priority creditors’. It can occur both when a company is able to pay its debts (i.e., it is ‘solvent’), and when it is chronically unable to do so (i.e., it is ‘insolvent’).

This ‘Ultimate Guide to Liquidation’ is split into three parts. This part, ‘Ultimate Guide to Liquidation Part 1: What is Liquidation’, explains in detail the process of liquidation in Australia. This includes:

- The definition of liquidation;

- The key elements of the main types of liquidation including members’ voluntary liquidation (MVL) and creditors’ voluntary liquidation (CVL);

- The new simplified liquidation process that has been introduced for small and medium-sized enterprises (SMEs);

- How liquidation compares to other insolvency processes;

- When a voluntary liquidator should not be appointed;

- The creditor power to request information from liquidators;

- The Fair Entitlements Guarantee (FEG) scheme for employees;

- The removal of the requirement for liquidators to hold ‘first meetings’ with creditors.

In the ‘Ultimate Guide to Liquidation Part 2: Preparing for Liquidation’, we look at:

- The fact that liquidations produce little return for creditors in Australia;

- The steps that small and medium-sized enterprises need to take to prepare for a voluntary liquidation;

- How directors should go about choosing the right liquidator;

- The situation where the courts appoint a liquidator over the top of an ‘11th hour’ voluntary administrator.

In the ‘Ultimate Guide to Liquidation Part 3: Responding to liquidation’, we consider:

- How liquidators go about charging fees;

- How conduct of a liquidator can be reviewed;

- The steps to take to replace a liquidator;

- What directors of a company should do to minimise the fallout from a liquidation.

What is liquidation or winding up?

The terms ‘liquidation’ and ‘winding up’ are often used interchangeably. However, strictly speaking, under the Corporations Act 2001 (Cth), it is the overall process of ending a company that is ‘winding up’. Liquidation, by contrast, is the specific step of turning the remaining assets of the company into cash (making them ‘liquid’). The entire process is overseen and carried out by an individual called a ‘liquidator’. However, as is common in discussion of this topic, for the remainder of this guide we use the terms ‘winding up’ and ‘liquidation’ interchangeably.

So, why would a company be wound up?

Under Australian company law, the director or directors of a company have ultimate ‘oversight’ over the company – the buck stops with them. This means, directly or indirectly, they are often the ones pushing to end a company through a liquidation process.

Other key players in the life and death of a company, are the ‘officers’ and the ‘members’. Officers manage, and carry out day-to-day business operations on behalf of directors (for example, the CEO and CFO are usually officers). Members typically own shares in the company, and make decisions on important matters, such as changes to the company constitution and decisions to wind up a company. This is achieved via ‘special resolutions’ of the members.

Directors, officers and members all have rights and obligations under legislation, regulations, company constitutions and by-laws. The reality for SMEs (businesses with less than 200 employees), is that the directors, officers and members are the same people or at least members of the same family.

There are many reasons why directors of an otherwise successful company may wish to end that business by appointing a qualified individual (a liquidator) to finalise the company’s affairs and liquidate its remaining assets: the legal procedure known as ‘liquidation’. For example,

- Sale of business through the sale and purchase of assets (as opposed to the sale of a business through the acquisition of shareholding) and the existing company no longer trading;

- The purpose for the existence of the company has ceased;

- A restructure of a group of companies whereby a subsidiary is voluntarily wound up.

At other times, the business may not be going so well. It may be insolvent, or on the brink of insolvency. At this point, directors are forced to seriously question the continued existence of the company. This is because:

- Directors can be found personally liable for continuing to trade while insolvent;

- Directors could have personal liability for tax debts via a ‘Director Penalty Notice’ issued by the Australian Tax Office.

Liquidation is not the only formal legal mechanism for ending the existence of a company: They can also be de-registered. However, while it is a relatively straightforward process, the following conditions must be met before doing so:

- All members must agree to doing so;

- The company must no longer be trading;

- Assets must be worth less than $1,000;

- There must be no outstanding debts or liabilities;

- The company must not be involved in any outstanding court proceedings; and,

- The company must have paid all outstanding fees and penalties.

As it is rarely the case that a recently trading company will be in this position, a voluntary liquidation is usually a necessary first step towards de-registration of the company.

For more information on this process see the Australian Securities & Investment Commission’s How to apply for voluntary deregistration.

If directors do not take seriously the decision to end the company and the question of solvency, there is a risk that a court will find them insolvent, and they will be subject to a compulsory liquidation. When this occurs, the court appoints a liquidator to supervise the winding up of the company by application of the creditors, members, the liquidator or a regulator.

Voluntary liquidation and insolvency

There are two main types of voluntary liquidation: a members’ voluntary liquidation (‘MVL’) and a creditors’ voluntary liquidation (‘CVL’). There is also a new, special type of CVL called a ‘simplified liquidation’ which is discussed in further detail in section 8 of this article.

Under section 494 of the Corporations Act 2001 (Cth), an MVL requires that a majority of directors make a ‘declaration of solvency’. If directors consider that the company is insolvent, and they seek to liquidate, they must initiate the CVL process, rather than the MVL process.

The question of solvency/insolvency is not just about which kind of liquidation must be carried out, however. It also impacts on the personal liability of directors for insolvent trading, and the possibility of another formal insolvency appointment such as a ‘voluntary administration’.

In light of the importance of solvency and insolvency, what exactly is the difference?

Section 95A of the Corporations Act 2001 (Cth) defines solvency and insolvency as follows:

- A person (including a company) is solvent if, and only if, the person is able to pay all the person’s debts, as and when they become due and payable.

- A person who is not solvent is insolvent.

According to the decisions of Courts (‘common law’), there are two tests for insolvency.

- The cash-flow test: assesses the ability of a company to pay its debts (or sell its assets fast enough to pay its debts) as they become due and payable;

- The balance sheet test: assesses the solvency of a company in reference to the total external liabilities against the total value of company assets. If liabilities exceed assets, the company is insolvent.

The cash-flow test is the principal test used by the Courts because it follows more closely the section 95A definition above. It requires an analysis of:

- The company’s existing debts;

- Whether the company’s debts are payable in the near future;

- The date each debt will be due for payment;

- The company’s present and expected cash resources; and

- The dates any company income will be received.

A key takeaway from the definition of insolvency is that it may not be obvious whether a company is solvent or insolvent. It is not enough to have a ‘temporary lack of liquidity’; there must be an ‘endemic shortage of working capital’ as per the decision in ASIC v Plymin (2003).

Note that up until December 31 2020, under COVID-19 insolvency law changes, there will usually be a longer period in which to ascertain whether a company is solvent or not. The increased time period (from 21 days to 6 months) for a business to respond to a ‘statutory demand for payment’ from a creditor, means a much longer period is required before the company can be ‘deemed’ insolvent. This makes it more difficult for an unpaid creditor to establish insolvency and initiate a compulsory liquidation. In addition, these changes mean that the amount owing must be $20,000 (rather than $2,000), before the demand for payment may be made.

This may be a relevant factor for directors themselves in establishing whether the business is solvent – capable of paying debts as they fall due.

Note also that under the new restructuring process (see section 7 of this Part), there is a stay on issuing statutory demands to companies that are waiting to undergo a restructuring process.

The key elements of a members’ voluntary liquidation (MVL)

As mentioned, in an MVL, the directors make a ‘declaration of solvency’ which gets the ball rolling. A meeting is then called of the members of the company to resolve by ‘special resolution’ (75% of members who attend the meeting voting in favour), to wind up the company: see section 491 of the Corporations Act 2001 (Cth).

Accompanying the declaration of solvency which is sent to members, must be a copy of the company’s statement of affairs. The declaration is required, pursuant to section 494(3) of the Corporations Act 2001 (Cth), to be:

- Made at the meeting that considers the MVL;

- Lodged with Australian Securities & Investments Commission (‘ASIC’) before notice of the meeting is given; and,

- Made within 5 weeks of the date of the resolution to give effect to the MVL.

If these requirements are not met, the declaration of solvency will be ineffective and the winding up of the company will not be an MVL.

If the above requirements are met, and a company is successful in passing a resolution for a MVL to take place, a voluntary liquidator will be appointed. Normally, pursuant to section 532 (1) and (2) of the Corporations Act 2001 (Cth), an appointed liquidator of a company must be a registered liquidator and be independent of the company.

However, pursuant to section 532(4) of the Corporations Act 2001 (Cth), if a company is a proprietary company and the winding up is an MVL, the appointed voluntary liquidator is not required to be a registered liquidator and can be an officer of the company or other professional with the necessary expertise.

The key elements of a creditors’ voluntary liquidation (CVL)

A CVL, unlike an MVL, occurs when a voluntary liquidator is appointed to an insolvent company. Although a CVL is described as a ‘creditors’’ winding up, the creditors of a company are in fact unable to commence a CVL and they are usually instigated by the company director(s).

If a director forms the opinion that the company is insolvent (i.e. unable to pay debts as they become due and payable, see section 95A) and no declaration of solvency can be made, they can convene a meeting of members and resolve to pass a special resolution (75% of members after quorum is needed), to wind the company up. Creditors are not required to attend the meeting where it is resolved to wind up a company.

At the meeting, the company will appoint a voluntary liquidator. The appointed creditors’ voluntary liquidator in these circumstances, as referenced above, must comply with section 532 (1) and (2) of the Corporations Act 2001 (Cth) and be a registered liquidator and independent from the company.

Although the appointment of a creditors’ voluntary liquidator through the determination of insolvency by a director is the most common type of CVL, there are other ways that the liquidator can be appointed. These include:

- The members’ voluntary liquidator appointed under an MVL determines that the company is actually insolvent and the appointment of a creditors’ voluntary liquidator is required;

- Transition from voluntary administration to a CVL; and

- ASIC appointment.

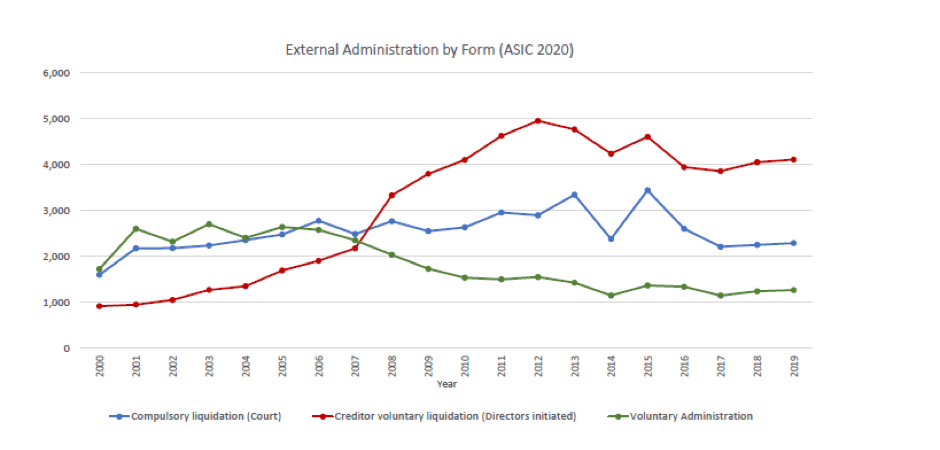

How MVLs and CVLs compare to other insolvency processes

Voluntary liquidation is not the only formal insolvency appointment available to directors when a company is financially struggling. Some might consider ‘voluntary administration’: A process where an independent professional takes control of an insolvent or near-insolvent company with the goal of coming to a successful ‘Deed of Company Arrangement’ or ‘DOCA’ with creditors to settle their outstanding claims.

The chart below compares the rates of different types of insolvency with voluntary administrations. As you can see, CVL is more-or-less four times more common than a voluntary administration.

Why is this? It might be that, by the time that a company seeks advice on a formal insolvency appointment, it is in so much difficulty that winding up is inevitable. Or, it could be that a voluntary administration is interpreted as a “glorified liquidation” anyway, in which case going straight to liquidation would reduce formal appointment costs. For more information see The Complete Guide to Voluntary Administration.

The new formal debt restructuring process

We have been suggesting for a while that the existing formal insolvency processes are inadequate, and that there needs to be tailored processes in place to support turnaround for SMEs. Finally, at the push of COVID-19, the Commonwealth Government has introduced such a process. This process establishes a new role of a ‘Small Business Restructuring Practitioner’ (‘practitioner’) who will oversee a formal restructuring. In short:

- A small business in financial difficulty approaches a practitioner to discuss a possible restructure;

- If appropriate, the practitioner advises that re-organisation is appropriate and proposes a flat fee for completing the work;

- By a resolution of the directors, the company appoints the practitioner. From this point unsecured creditors cannot take action against the company, personal guarantees cannot be enforced and protection from ipso facto clauses apply;

- The business owners/directors work with the practitioner to develop a restructuring plan. They have 20 days to do so. If satisfied, the practitioner can ‘certify’ that plan;

- Both the plan and associated documents (such as the practitioner’s fees and expenses) are sent to creditors;

- Creditors vote on whether to accept the plan and proposed remuneration and have 15 days to do so. Where more than 50 per cent of creditors by value agree to the plan, it is approved and then applies to and binds all unsecured creditors;

- Once (and if) approved, the business will continue to trade with the practitioner making the required distributions under the plan.

- If the creditors do not approve of the plan, the process ends and directors must decide whether to go into liquidation. Note, in many cases, the business will be eligible for ‘simplified liquidation’ (see below).

To read more about this process see Insolvency Revolution for SMEs: Australia’s new ‘debtor in possession’ restructuring procedure

The new simplified liquidation process for small businesses

It has been evident for a long time that Australia’s ‘one-size-fits-all’ liquidation model is inappropriate for SMEs. This inadequacy has become particularly evident in the wake of the COVID-19 related economic turbulence. In response, the federal government has introduced a simplified liquidation process.

In overall structure, this new process is similar to existing liquidation processes, albeit with a range of changes made to speed up and reduce the cost of liquidation. As with a standard liquidation, small businesses will be able to appoint a liquidator to wind up the company and liquidate any remaining assets to distribute to creditors. The liquidator will still have the capacity to investigate potential wrongdoing and report to creditors.

This process will be available for companies with liabilities totalling less than $1 million.

The liquidator will also still investigate and report to creditors about the company’s affairs and inquire into the failure of the company. Key changes from the normal CVL process include:

- Fewer situations are permitted where the liquidator is able to clawback ‘unfair preference’ payments. In a standard liquidation, liquidators have the power to pursue certain transactions entered into by the company which conferred a preference on one or some of the creditors, or provided a benefit to a related party or creditor to the detriment of other creditors. The goal is to increase the ‘pot’ of assets available for distribution. Regulations accompanying the new law will specify a smaller set of transactions that will be voidable in this way;

- An alteration to the rules around liquidator reporting. The liquidator will only be required to report to ASIC about potential misconduct where there are reasonable grounds to believe there was misconduct (see section 533 off the Corporations Act 2001 (Cth)). The mandatory reporting requirement in standard liquidations is time-consuming and expensive, significantly eating into the remaining assets that would otherwise be available for distribution to creditors;

- Removal of the liquidator’s requirement to call a meeting of creditors. In a standard liquidation, some creditors or ASIC are able to direct that a liquidator hold such a meeting. Instead of being required to convene a meeting, liquidators will be required to provide information to creditors, and put proposals to them, electronically;

- Removing the capacity for creditors to create committees of inspection. In a regular liquidation, creditors have the capacity to appoint a committee of inspection which oversees the liquidator process and has the power to approve liquidator fees and expenses;

- Removing the capacity for creditors to appoint a ‘reviewing liquidator’. We discuss the role of the reviewing liquidator further in the ‘Ultimate Guide to Liquidation Part 3: Responding to liquidation’. Note, the court will still retain its oversight powers, so it will be able to appoint a reviewing liquidator as required;

- Simplification of the dividend and proof of debt processes;

- Optimising technology neutrality for voting and other forms of communication.

Under certain circumstances, companies will exit the simplified liquidation process. This will occur where the liquidator becomes aware that the eligibility criteria are not met, or under another criterion specified in the regulations. This could happen, for example, where the liquidator becomes aware of an additional creditor meaning that the company no longer has less than $1 million in liabilities.

When the company is no longer eligible for the simplified process, they are transitioned into the standard liquidation process.

Note that various regulations associated with this process are yet to be confirmed, so certain elements of the simplified liquidation process could change.

Avoiding formal insolvency appointments

Whether a CVL, a voluntary administration or a compulsory liquidation, formal insolvency appointments usually mean the death of the business. While the new formal restructuring process offers some chance of helping SME directors turn their business around, it remains to be seen how successful that process will be. So, what is the lesson here?

There are several mechanisms currently available which may enable directors to put a plan together to save the company. These are:

- The COVID-19 Safe Harbour. The Coronavirus Economic Response Package Act provides a new temporary ‘safe harbour’. Directors will not be personally liable for insolvent trading where they meet the following conditions:

- the debt is incurred in the ordinary course of business;

- the debt is incurred in the six-month period from when the law comes into effect;

- the debt is incurred before the appointment of the voluntary administrator or liquidator.

Note, this safe harbour only applies up until 31 December 2020. After that point, the new ‘restructuring’ safe harbour applies instead.

- Standard Safe Harbour. This safe harbour was introduced in 2017, but not all directors understand its implications well. Under section 588GA of the Corporations Act 2001 (Cth) it provides that the duty of a director not to trade while insolvent does not apply if:

- at a particular time after the director suspects insolvency, the director develops a course of action that is reasonably likely to lead to a better outcome for the company; and

- the company debt is incurred in connection with the course of action.

Both the Covid-19 and standard safe harbours could be used in order to re-organise or restructure the business, such as through a ‘pre-packaged insolvency arrangement’ (‘pre-pack’). For more information see What you need to know before you pre-pack (to avoid phoenix activity).

- Restructuring Safe Harbour: Under the new restructuring provisions that come into effect on 1 January 2020, the duty of a director to ensure that the company does not trade while insolvent, does not apply:

- during the restructuring of the company; and

- in the ordinary course of the company’s business, or with the consent of the restructuring practitioner or by order of the Court.

When you shouldn’t appoint a voluntary liquidator – a checklist

We suggest that, before initiating the process for appointment of a voluntary liquidator, you consider the following checklist and do not appoint a voluntary liquidator if one of the criteria applies:

- As outlined above, if you plan to continue trading afterwards through buying assets from a liquidator. Instead, organise this before appointment through a pre-pack;

- If you have uncommercial transactions or unfair preference claims that can be made against you. In these cases, you need to see a lawyer first;

- If you have a directors’ loan account owing. This should be distributed as income first, or a lawyer should be engaged to look into it;

- If you haven’t vetted and qualified your proposed liquidator through a trusted source;

- If you haven’t considered an informal restructure first as an option;

- If you are an SME director and you have not considered the possibility of appointing a restructuring practitioner and going through a formal restructuring process;

- If the COVID-19 insolvency law changes are still in place and you have not sought advice on their application to your situation.

What is the creditor power to request information from liquidators?

In addition to the poor outcomes of liquidation for directors and creditors, a common complaint about liquidation in Australia has been the lack of transparency in the process. Many creditors have felt like there is inadequate disclosure by liquidators of key information. Prior to 2016, creditors were limited in their ability to hold liquidators to account via reporting and information gathering. This was improved in 2016 when a new insolvency framework was introduced to ensure that creditors have a right to request reports, documents and information from liquidators (whether individually or as a group).

This has been seen as an improvement on the pre-2016 framework which left creditors largely in the dark about key liquidation issues. We explain this power to request information below.

The problem: lack of disclosure

When a company is wound up, creditors do not (usually) appoint the liquidator, even though the liquidator is required to act in the interests of the creditors. In light of this, creditors often end up unsatisfied with the liquidation process. Their frustrations include:

- An overwhelming feeling of impotence in the liquidation process. Creditors may find their inquiries with liquidators stonewalled and suspect that the liquidators really work for the directors. This is usually untrue. However, liquidators are incentivised to maximise fees and carry out a liquidation as efficiently as possible. This may mean reporting to creditors is seen as an unnecessary hindrance;

- Creditors perceive liquidators as acting as an effective monopoly. With terms of engagement so common across liquidators, creditors don’t feel they can easily appoint a better alternative, and they know they are practically impossible to replace;

- Slow liquidations. Once appointed, liquidators have been known to take their sweet time – timeframe for liquidation is 1-2 years. Creditors sometimes cannot afford to wait this long to find out if they will get any money back.

In this section, we are focused on the information-gathering power available to creditors to manage their frustration with liquidators. However, it is worth noting that there are other mechanisms available to creditors for supervising liquidator conduct, including:

- removal of liquidators via a resolution of creditors;

- court applications for replacement of a liquidator;

- appointment of a ‘Reviewing Liquidator’;

- appointment of a committee of inspection.

The 2016 Rules

Creditors may now ask their liquidator for information, reports or documents under Division 70-40 (when acting collectively by resolution) or 70-45 (when acting individually) of the Insolvency Practice Schedule (Corporations). This right applies to creditors in a creditor’s voluntary winding up and ‘members’ in the case of a members voluntary winding up.

While our focus in this article is on the power of creditors to acquire information from liquidators, these provisions also apply in the case of voluntary administration.

Under 70-40(2) and 70-45(2) of the Insolvency Practice Schedule (Corporations), a liquidator must comply with this request except where:

- The information, report or document is not relevant to the liquidation;

- It would breach their duties as a liquidator;

- It would otherwise be unreasonable to do so.

The Insolvency Practice Rules (Corporations) 2016 set out the conditions under which a liquidator may hold that it is not reasonable to comply with the request. We will look at this power later in the article.

Pre-2016 creditor information powers

Prior to the introduction of the Insolvency Practice Schedule (Corporations) and Insolvency Practice Rule (Corporations) 2016, what options were available for creditors who required information? The key mechanisms were:

- Compulsory reporting processes. These were concerned primarily with directors reporting to liquidators and ASIC (e.g. in the Report as to Affairs (RATA) now replaced with the Report on Company Activities and Property ROCAP). While liquidators were expected to provide written reports to creditors, this often didn’t happen;

- Right to view the liquidator’s books. Liquidators had (and still have) a right to inspect the liquidators’ books, which in turn must be up-to-date and accurate. This requires significant effort on behalf of the creditor and is not a general right to information;

- Powers of the committee of inspection. Creditors can choose to appoint a ‘Committee of Inspection’ early in the liquidation process who represent the creditors and can direct the liquidators to act in various ways. Note, however, that the liquidator is not generally bound by the directions of the committee of inspection.

How is the power to request information useful?

The limits of committees of inspection and existing reporting processes meant that, in reality, creditors were limited in their ability to supervise the liquidation process. In addition to improving the tools available to creditors, the new right seeks to:

- Enable creditors to ensure that liquidators are acting in their interests as required to by law;

- Enable creditors to supervise the liquidator’s costs themselves;

- If there is a prospect of future litigation, provide an alternative to discovery in expensive court action. This was confirmed recently in In the matter of 1st Fleet Pty Ltd (in liquidation) [2019] NSWSC 6.

Liquidator’s right to refuse

The creditor’s right is only a right of request. As set out above, there are specific grounds under which the liquidator can refuse to comply under the Insolvency Practice Rules (Corporations) 2016. The most significant of those grounds for refusal are set out in 70-10 of the Insolvency Practice Rules (Corporations) 2016. A liquidator can refuse the request if:

- complying with the request would substantially prejudice the interests of one or more creditors or a third party and that prejudice outweighs the benefits of complying with the request;

- the information is privileged;

- disclosure could be a breach of confidence;

- insufficient available property to comply with the request;

- the information, report or document has already been provided; or

- the information, report or document is required to be provided under the Corporations legislation within 20 business days of the request being made; or

- the request is vexatious.

These grounds significantly limit the liquidator’s power of refusal. In the relatively recent case, In the matter of 1st Fleet Pty Ltd (in liquidation) [2019] NSWSC 6, the court overruled a liquidator’s decision to refuse to provide information on the grounds that they had already provided that information to the committee of inspection. As the prior provision of the information to another party is not a specified ground for refusing to provide information, the liquidator could not refuse on those grounds.

Conclusion – the power of the power to request information

The new power for creditors to request information for liquidators puts significant power back in the hands of creditors. While liquidators do have the power to refuse to provide that information, the grounds for refusal are significantly limited.

What is the Fair Entitlements Guarantee (FEG) scheme?

As discussed, the returns for unsecured creditors in liquidation in Australia are abysmal. Sadly, this often leaves employees out of pocket. In response there is a scheme to support employees known as the Fair Entitlements Guarantee (or ‘FEG’) scheme.

The FEG Scheme, previously known as the General Employee Entitlements and Redundancy Scheme (GEERS) is available to all eligible employees to ensure they get (some) of what they are entitled to. The FEG Scheme provides for:

- Unpaid wages of up to 13 weeks (capped at a maximum weekly wage, currently set at $2,451);

- annual leave;

- long service leave;

- payment in lieu of notice of termination set at a maximum of 5 weeks;

- redundancy pay of up to 4 weeks per full year of service.

Note, that the FEG Scheme does not cover all employee entitlements. It does not cover:

- superannuation;

- reimbursement payments;

- one-off or irregular payments;

- bonus payments;

- non-ongoing or irregular commissions.

For more information on the FEG Scheme see the Fair Work website.

The FEG scheme, as a scheme of last resort, is intended only to apply where there are insufficient assets to pay out employee entitlements. Note also that there are eligibility restrictions. The restrictions include the scheme not applying to contractors and those who have been directors of the company within the last 12 months, among other conditions.

There has been a concern in recent years that companies have been misusing the FEG Scheme, including the occurrence of ‘illegal phoenix activity’, where assets have been transferred out of the company prior to insolvency which would have otherwise been used to pay employees their entitlements.

Contractors are not employees

As contractors are not employees, they are simply ordinary unsecured creditors when it comes to the winding up of the company. This means that (a), they have no priority in liquidation and (b), they have no access to the FEG Scheme. This means that the following question becomes crucial: is a given individual an employee or a contractor? The answer does not depend simply, on whether there is an employment agreement or contract in place. There is no hard-and-fast rule determining whether a given person falls into one category or the other. However, for tax and superannuation purposes, the Australian Tax Office (‘ATO’) considers the following factors determinative:

- Ability to subcontract/delegate: An employee generally cannot subcontract/delegate their work, but a contractor can;

- Basis of payment. An employee is paid either for the time worked, a price per item or activity or a commission, whereas a contractor is paid for a result achieved;

- Equipment, tools and other assets. Employees are usually supplied equipment and tools whereas contractors usually supply their own;

- Commercial risks. The worker takes no commercial risks as the business is responsible for the work done and rectifying it. Contractors take commercial risks and are responsible for rectifying any defects in work completed;

- Control over the work. The business has the right to direct employees in how they get their work done, whereas a contractor has considerable freedom in how they complete the work;

- The worker is part of the business whereas the contractor operates an independent business and is free to accept or refuse additional work.

For further information check on the ATO website.

Options for contractors

As the majority of liquidations in Australia result in very few assets remaining to distribute to unsecured creditors, this will often mean unsecured creditors walk away from a liquidation empty-handed. In light of this, it is important that contractors take into account this commercial risk when they enter into a contract and frame their prices accordingly. In addition, it may be possible in some cases for contractors to secure their debts through registration of a security interest (e.g. over the equipment of the debtor company).

Once winding up is underway, what options are open to the contractor to get what they are owed? Options for contractors are limited, but matters worth considering include:

- Making a claim of ‘sham contracting’. Considering the factors outlined in section three, ‘contractors’ might consider whether they are in fact employees and therefore entitled to priority in liquidation and/or access to the FEG Scheme.

- Using creditors’ remedies to increase the pool of remaining assets. An ‘unfair preference’ claim might be made where one creditor (such as a contractor) has been discriminated against in favour of another contractor. This can occur when the company has made payments to one creditor prior to winding up where the company was already insolvent.

Voluntary liquidators no longer required to hold first meetings

Formerly, it was a requirement in an MVL that, if the directors of the company were not prepared to make a declaration of solvency, a first meeting of the creditors had to be called by the liquidator. At this meeting, the liquidator could be replaced.

As a result of changes to the law in 2016, this meeting is no longer required. However, in its place, there are new reporting requirements and a power for creditors to call a meeting at any time.

There are pros and cons to this change depending on your perspective, but if it works as intended, the MVL process will be streamlined. We explain how the new process works below.

Note, in the simplified liquidation process (a type of CVL), there is also no requirement to hold meetings.

What is a voluntary liquidation and how is one initiated?

A voluntary liquidation occurs when the members (i.e., the shareholders) or the creditors of a company, rather than the court, resolve to a wind up a company. Recall that an MVL may be initiated where the shareholders of the company (‘the members’) resolve to wind up the company, but the company is not insolvent. This might be initiated, for example, in the case of company restructuring. This process generally requires that the Board declare the company to be solvent, though we will discuss the exceptions to this below.

The old rule: A first meeting must be called

Former section 497 of the Corporations Act 2001 (Cth) (now amended), required that, where there was no declaration of solvency by the directors, the members could still resolve to appoint a voluntary liquidator by special resolution. However, in that case, a meeting of the creditors had to be called no later than 11 days from that members’ meeting to decide, among other things, whether the liquidator would be replaced by creditors. At this meeting, the creditors could also determine whether to appoint a committee of inspection to oversee the work of the liquidator.

An equivalent duty to call a first meeting of the creditors still exists for voluntary administrators. You can read more about this process in our guide to voluntary administration.

The new rule: First meeting no longer compulsory

The requirement to hold a first meeting of creditors for an MVL has now been eliminated by virtue of the Insolvency Law Reform Act 2016. However, in its place there is an ability for creditors to call a meeting at any time. At one of these meetings the creditors can replace a voluntary liquidator.

Note, however, that the liquidator can refuse to hold such a meeting where they consider the request is not reasonable (See section 75-250 Insolvency Practice Rules (Corporations) 2016).

While there is no compulsory meeting requirement, there is still a reporting requirement which requires two documents to be prepared and provided to creditors in prescribed forms:

- a summary of the affairs of the business; and

- a list of the names and details of creditors, including any that are related entities of the company (see section 75-250 Insolvency Practice Rules (Corporations) 2016).

Both these documents must then be lodged with ASIC.

Just as with the ROCAP – Report on Company Activities and Property for voluntary administrators, this reporting is designed to provide output of the earliest investigations by the liquidator into the company. It may also deliver insight into whether inappropriate behaviour, such as phoenix activity, has been occurring or is about to occur.

Pros and cons of the new rule

Is the new rule a good thing or a bad thing? It depends who you ask. Here we set out some of the pros and cons of the new rule from the perspective of both the directors of the company and the creditors:

- Pro for the company: As a meeting does not occur automatically, this may mean that for MVLs there is a reduced likelihood of the directors’ choice for liquidator being replaced;

- Pro for the company: As there is a reduced likelihood of a meeting being called, this may reduce the pressure on directors to make a declaration of solvency when they don’t feel comfortable in doing so;

- Pro for creditors: There is now an ongoing power to call a meeting to replace the liquidator. This means that if creditor concerns with the liquidator arise during the liquidation there will be a remedy available;

- Pro for both: Meetings can be a significant expense and, in many cases, there are limited assets to be distributed. If there is no desire for a meeting to be called by any parties then it is to the benefit of all that there is no meeting;

- Con for creditors: The ability of the liquidator to refuse to convene a meeting could still be a significant barrier to a creditor calling a meeting at a later stage. This may make it more difficult to organise other creditor-friendly interventions such as a committee of inspection.

Conclusion of part one

To summarise the liquidation process as discussed in part one of this ‘Ultimate Guide to Liquidation’:

- The decision of whether or not to appoint a voluntary liquidator (or initiate the process), is a serious one for directors and it needs to be pursued with caution;

- The type of liquidation that is initiated, MVL or CVL, depends on whether the company is solvent (and whether directors are confident to make a declaration to that effect);

- A key difference between MVLs and CVLs is that the liquidator in an MVL is cheaper;

- Voluntary liquidations are four times as popular as voluntary administrations which may relate to the generally poor success rates of voluntary administration;

- The new simplified liquidation procedure may increase the likelihood of returns for unsecured creditors of small businesses.

In order to avoid liquidation, businesses might consider:

- Whether a ‘standard’ safe harbour or ‘COVID-19’ safe harbour protections might be employed to pursue informal restructuring solutions such as ‘pre-pack’ arrangements;

- From 1 January 2021, whether or not they are eligible for the new restructuring process for SMEs.

Key details of the liquidation scheme in Australia that all directors and creditors should be aware of includes:

- The Fair Entitlements Guarantee (FEG) scheme;

- The power of creditors to request information from creditors;

- The removal of the requirement for liquidators in an MVL to hold a first meeting with creditors.

In Parts 2 and 3 of the Ultimate Guide to Liquidation we look at how businesses can prepare for liquidation, and how they can respond once liquidation is initiated.