What you need to know before you pre-pack (to avoid phoenix activity)

DownloadWhite Paper for professional advisers of SMEs about pre-pack insolvency arrangements

By Ben Sewell, Sewell & Kettle Lawyers

Date of update: July 2020

Overview

- What is a pre-pack insolvency arrangement?

- Who should read this White Paper?

- What is a pre-pack voluntary administration?

- Who is a pre-pack insolvency arrangement suitable for?

- What is the safe harbour from insolvent trading?

- What is phoenix activity?

- Why is the ASIC, the ATO and Department of Employment becoming more active in pursuing phoenix activity?

- What is the difference between a secured and an unsecured creditor?

Insolvency issues for SMEs

- What are SMEs and why are they important?

- What financial and operational issues do SMEs face?

- What is the legal meaning of insolvency?

- What are the indicators of insolvency recognised by Courts?

Directors and advisors of SMEs

- What are the principal legal duties of directors?

- What is insolvent trading?

- How does a director get a safe harbour protection from insolvent trading?

- Why do directors need to watch out for Director Penalty Notices (DPNs) from the ATO?

- What penalties can directors face for insolvent trading and breach of duty?

- What immediate actions should directors of an SME take if their company is insolvent?

- What types of professional advisors assist with a pre-pack insolvency arrangement?

- What are the duties of professional advisors advising insolvent SMEs?

Liquidators of SMEs

- Who are liquidators and what do they do?

- What is the downside of a liquidation firesale?

- When can a liquidator claw back transactions made to related entities, including a new company?

- What factors do liquidators take into account when they decide whether to pursue illegal phoenix activity?

Voluntary administrators of SMEs

- What is voluntary administration?

- Why do SMEs appoint voluntary administrators?

- What are the downsides of voluntary administration?

- Why is voluntary administration impractical for a microbusiness (1-4 employees)?

- Are insolvency practitioners under a conflict of interest when advising on a pre-pack voluntary administration?

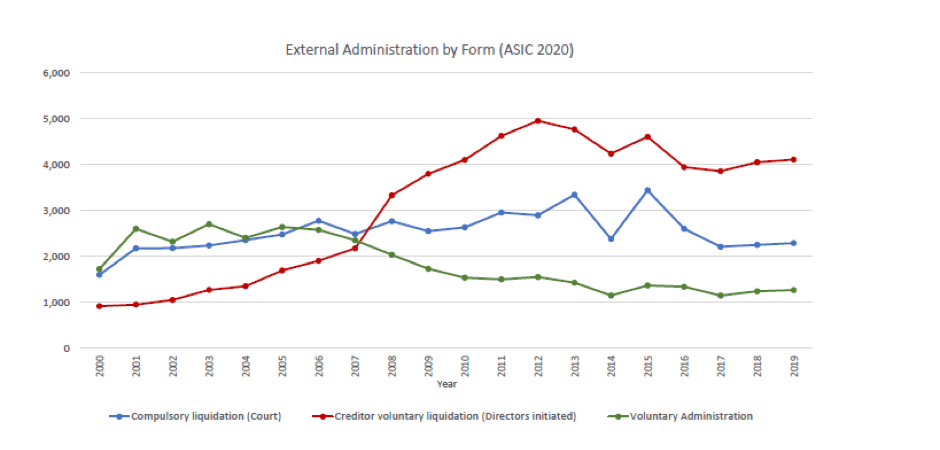

- What are the future prospects of voluntary administration: are results improving or declining?

Restructuring of SMEs

- What is informal restructuring?

- How does a director obtain safe harbour protection from insolvent trading?

- What does the law consider to be phoenix activity?

- When can an insolvent business be transferred to a related entity?

- How does Fair Entitlement Guarantee treat employees when a business is liquidated?

- If employees are transferred from a company in liquidation, do employee entitlements transfer?

- How can directors be penalised for phoenix activity and utilising FEG to pay outstanding entitlements?

- What does the licensing of a business mean?

- What types of finance are available for a pre-pack insolvency arrangement?

- Why are pre-pack insolvency arrangements common-place restructuring transactions in the UK but not in Australia?

- What standards of valuation do courts expect for pre-pack insolvency arrangements?

- Are pre-pack insolvency arrangements possible if there are secured creditors?

- What operational improvements can result from a pre-pack insolvency arrangement?

- Are pre-pack arrangements possible if premises and/or plant and equipment are all leased?

- What do the courts regard as a sham or fraudulent transaction?

- Capstone comment: Why is it difficult to successfully execute a pre-pack insolvency arrangement?

Overview

What is a pre-pack insolvency arrangement?

The market for insolvency services is shrinking, and particularly with small-to-medium sized enterprises, lower cost and less disruptive methods for rescuing insolvent businesses are becoming the focus of the profession. There has been 25 years without a recession and financiers are generally reluctant to appoint receivers so there is simply less work for insolvency practitioners.

The pre-pack insolvency arrangement is an opportunity to achieve a business rescue without the cost and disruption of a voluntary administration. It is an example of an informal work-out methodology.

A pre-pack insolvency arrangement is an instrument for rescuing an insolvent business through a legally binding transaction either before or after the formal appointment of an insolvency practitioner. It is an alternative to using voluntary administration for rescuing an insolvent business from a liquidation fire sale.

The methodology of using a private treaty to rescue an insolvent business without principally resorting to a formal insolvency appointment is not new. Illegal private treaty arrangements, originally “bottom of the harbour” schemes and now “phoenix activity” contrast with legal pre-pack insolvency arrangements. The purpose of this White Paper is to help professional advisers to understand alternative approaches to informal work-outs without resorting to phoenix activity.

The terms “pre-pack”, “pre-pack insolvency” and “pre-pack arrangement” are interchangeable but “pre-pack insolvency arrangement” will be used in this discussion paper. This discussion is focused on legal pre-pack arrangements and helping directors and entrepreneurs to avoid litigation and fall out from both poor quality and illegal advice that can lead to phoenix activity.

The essential preconditions for a pre-pack insolvency arrangement are that a business is insolvent and that the directors have an intention to restructure their affairs to rescue the business. Pre-packs may also apply to sole traders and partnerships but these vehicles for trading have been largely overtaken by the corporate form (i.e. a proprietary limited company) so sole traders and partnerships are not discussed in this paper. Sole traders and partnerships are only prevalent now in industries where professionals are prohibited from trading through corporate entities.

A pre-pack insolvency arrangement has the following elements:

- A company (Oldco) is insolvent;

- Oldco’s business is transferred for commercial consideration to a related entity (Newco); and

- The transaction betweenOldco and Newco results in an optimal outcome for stakeholders.

There are two types of pre-pack insolvency arrangements:

- The transaction takes place after Oldco is placed in insolvent administration (i.e. liquidation or voluntary administration); or

- The transaction takes place before Oldco is placed in insolvent administration.

The pre-pack insolvency arrangement is not widely utilised in Australia but it has been recognised as a valid methodology by courts, the legal profession and government bodies. The pre-pack insolvency arrangement was acknowledged as a legitimate restructuring transaction in a recent government report into phoenix activity:

A genuine business failure where the business has been responsibly managed and subsequently continues using another corporate entity is a legitimate use of the corporate form. [1]

The insolvency profession is generally against promoting or utilizing pre-pack insolvency arrangements. The focus of the Australian insolvency regime has been to have an independent insolvency practitioner appointed over insolvent companies through a formal restructure process (i.e. a voluntary administration). It is understandable that insolvency practitioners would resist informal arrangements, because it results in less profitable work and a loss of control over the insolvency process. However, professional advisers should be aware that if a company is insolvent, at some point in time it may ultimately be placed in liquidation and at that time the insolvency practitioner appointed will have the task of reviewing the pre-pack insolvency arrangement. Therefore, it is essential for any director undertaking an informal work-out and asset transfer to strictly comply with their legal obligations or they may face a claw-back action by a liquidator down the track.

Who should read this White Paper?

The purpose of this White Paper is to inform small-to-medium sized enterprise (SME) directors and their professional advisors about pre-pack insolvency arrangements and the consequences of poor restructuring advice.

The White Paper is also a challenge to phoenix activity promoters whose illegal advice has expensive consequences of personal liability for tax debts and the continuation of unsustainable business. It is not in anyone’s interest to continue a loss-making business and directors are better off doing something else!

SMEs are businesses employing less than 200 people and these businesses represent 99.7% of businesses in Australia. SMEs have unique needs because they have small shareholdings (i.e. usually an entrepreneur or a family), they are sensitive to professional fees and often have poor business processes and records. SME professional advisors need to have a “whole of business” approach to identify obstacles including personal, operational and financial difficulties that their clients face. This information should then be utilised when developing a rescue strategy.

This White Paper is relevant for a range of people involved with SMEs, including:

- SME directors;

- Accountants;

- Insolvency practitioners;

- Property and transactional lawyers;

- Family and estate planning lawyers; and

- Insolvency lawyers.

This is not a “tips and traps guide” or “7 things you must do to implement a pre-pack rescue”. There is no single accepted methodology for planning and implementing a pre-pack insolvency arrangement because of the complexities of tax law and corporate law, and market realities faced by SMEs.

Best of luck working on your turnaround! On the other hand, remember that you can arrange for an orderly liquidation through the safe harbour protection in the event that a pre-pack insolvency arrangement isn’t feasible.

What is a pre-pack voluntary administration?

A pre-pack voluntary administration occurs when there is an arrangement (i.e. a restructuring plan) planned before the appointment of a voluntary administrator. The arrangement is likely to include the transfer of business assets from OldcotoNewco, but the transaction may be completed either before or after the appointment of the voluntary administrator.

The primary difference between a pre-pack voluntary administration and a ‘regular’ voluntary administration is that in a pre-pack arrangement, the planning and negotiation of the business transfer takes place prior to the appointment of the voluntary administrator. Valuations would have already been obtained, contracts drafted and the sale price agreed upon before the appointment of a voluntary administrator in a pre-pack scenario.

In a ‘regular’ voluntary administration, the voluntary administrator takes over the management of the insolvent business and only begins sale or payment negotiations with stakeholders after their appointment. The directors put a proposal for a deed of company arrangement (DOCA) to the voluntary administrator. It was the intention of the creators of voluntary administration that the appointed insolvency practitioner would take “full control” of the insolvent company’s property. [2] It was not contemplated by the creators of voluntary administration that directors would execute a pre-pack before appointing a voluntary administrator because the DOCA proposal was intended to cover the entire restructure of an insolvent company.

After assessing the viability of the business, the voluntary administrator decides whether to continue trading under the business during the administration period or to close it down. There is a second meeting of creditors that decides the future of the business and whether creditors will accept a compromise, or put the company into liquidation.

The DOCA is the primary binding instrument between the creditors, directors and the voluntary administrator for any compromise arrangement made. A DOCA proposal is subject to a vote of creditors and therefore needs creditor support. The principal benefit of a DOCA for the directors is that the company does not go into liquidation and therefore, there are no claims for insolvent trading, uncommercial transfers or unfair preferences that can be made against them or related parties.

The obvious benefit of a pre-pack insolvency arrangement is that the directors of the insolvent business retain control of the restructure before the commencement of a formal insolvency (through a liquidation or voluntary administration). This is the case for a pre-pack transaction executed before the appointment of a voluntary administrator or liquidator. On the other hand, if the pre-pack transaction is not executed before the appointment of a voluntary administrator it is a matter of independent judgment as to whether the voluntary administrator finalises the transaction without the approval of creditors. There may be a number or reasons why a voluntary administrator would or would not sign off on a transfer before it is voted on by creditors. One reason would be that the voluntary administrator is not convinced that the price of the transfer could not be bettered through a public tender.

There is no “bidder’s tension” in a pre-pack scenario. In a “regular” voluntary administration, the voluntary administrator will evaluate any purchase offer of the business assets and will be unlikely to approve a sale before it is considered by the second meeting of creditors.

Who is a pre-pack insolvency arrangement suitable for?

Two key characteristics of an insolvent SME that qualify it for a pre-pack insolvency arrangement are:

- That there is a serious commercial issue with the goodwill in a business being damaged by a formal appointment scenario; and/or

- The costs of a voluntary administration are uncommercial.

The goodwill of a business is the value of a business over and above the price of all the assets of the business when broken up. Accountants would say that goodwill amounts to the excess of the “purchase consideration” (i.e. the price someone is willing to pay to purchase the assets of the business) over the total value of the assets. If a formal appointment (i.e. a liquidation or voluntary administration) is likely to damage goodwill or otherwise significantly reduce a potential purchase price of the business this is a valid commercial justification for a pre-appointment transfer of the business of Oldco to Newco.

In a liquidation scenario, the liquidator is under no obligation to continue trading a business and if they do, they are at personal risk if a liquidation trade-on suffers a loss. As a result of liquidation, the business may be terminated or put on hold, significantly impacting if not eliminating the goodwill value of the business. The liquidation of a company is likely to result in the total loss of a company’s goodwill. To avoid such a scenario, however, a liquidator does have the right to licence the business as a means of ensuring its continuity.

It is likely that the damage to goodwill value will have already been done by notification of the liquidation or voluntary administration to the suppliers and customers.

There is currently very little empirical research into the costs of voluntary administration but it may be observed that the professional costs of voluntary administration are on the rise. It may be expected that voluntary administration for an SME will cost between $50,000 and $200,000. One researcher found that even small voluntary administrations had average fees of $97,000. [3]

It is often uncommercial to appoint a voluntary administrator to a company, particularly in the case of microbusinesses with 1-4 employees and SMEs, as the costs could consume all the value in the business solely in administrator’s fees.

Pre-packs are quicker sales where the insolvent company (i.e. Oldco) can usually continue trading through Newco without going through a voluntary administration process. This would enable the company to retain the value of their brand, their employees and key customers.

What is the safe harbour from insolvent trading?

The safe harbour from insolvent trading is a protection to company directors from an insolvent trading claim run by a company liquidator. Under section 588G of the Corporations Act, company directors are under a duty to prevent their company from incurring debts whilst insolvent. This is a director’s duty, and the penalty for breaching the duty includes paying compensation.

Under the prohibition, a director of a company may become personally liable for debts incurred by their company whilst it is insolvent. Broadly, section 588G provides that a director will be found to have breached their duty if:

- The person was a director at the relevant time;

- The company was actually insolvent;

- The company incurred a debt; and

- There were reasonable grounds for the director to suspect insolvency.

The penalties for a director breaching the prohibition include:

- Civil penalties of up to $200,000 (sections 1317E and 1317G);

- Liability to compensate the company or relevant creditor for the amount of the debt incurred as a result of the breach (section 588M); and

- Criminal prosecution in limited circumstances (section 1311, Schedule 3 Item 138).

The safe harbour law provides that the duty to prevent trading while insolvent will not apply when:

- At a particular time after the director suspects insolvency, the director develops a course of action that is reasonably likely to lead to a better outcome for the company; and

- The company debt is incurred in connection with the course of action. [4]

To claim the safe harbour protection there is no specific process that is mandated for a director to undertake and it is dependent on the size and complexity of the company’s circumstances. But the safe harbour law includes indicators about what a course of action may involve, including the director (and therefore the board):

- Informing themselves about the company’s financial position;

- Taking steps to prevent misconduct by officers and employees;

- Keeping appropriate books and records;

- Obtaining advice from an “appropriately qualified entity”; and

- Developing or implementing a plan for restructuring the company.

The key test to be considered is whether the course of action developed may be “reasonably likely to lead to a better outcome for the company” (section 588GA(1)(a)). A “better outcome” is compared to what would occur if there was to be an immediate appointment of a voluntary administrator or liquidator over the company.

There are hurdles to obtaining the safe harbour protection and these include lodging tax returns and paying employee entitlements.

It should also be noted that the safe harbour protection has recently been amended as a result of the COVID-19 pandemic. The new Coronavirus Economic Response Package Omnibus Act 2020 (the Coronavirus Economic Response Act) has come into force and contains a range of new measures to support businesses through the Coronavirus/COVID-19 pandemic and its consequences. In particular, the Act creates a new ‘temporary safe harbour’ which protects directors from liability for insolvent trading while they respond to the Coronavirus pandemic and its consequences. This means directors don’t have to pull the trigger and appoint a voluntary administrator or liquidator, or at least not as quickly.

The take-away is that if directors take sensible steps to restructure a company informally they will be able to take advantage of the safe harbour. Directors need to develop a written plan that on balance would be likely to put the company in a better position than a liquidation or voluntary administration.

What is phoenix activity?

Phoenix activity is a loaded term that has connotations of fraud and acting selfishly and illegally by company directors and advisers. Unfortunately, there is no universally accepted definition in the law or an express definition in the Corporations Act that we can refer to. The reason there is no definition in the Corporations Act is that defining this concept is difficult and it would require an examination of the intentions of the directors.

Phoenix activity involves:

- An insolvent company (Oldco);

- The transfer of Oldco’s assets for inadequate consideration to a related entity (Newco); and

- The result is detrimental for creditors, employees and other stakeholders as they receive less than what they would have received from a voluntary administration or liquidation scenario.

There may also be a cyclical element because “phoenix operators” are the people who repeat this process for their own business or for clients who they provide sham labour hire arrangements for.

There is a recent research paper “Defining and Profiling Phoenix activity” that was released in December of 2014 that is the most thorough examination of the definition of phoenix activity by any academic to date. It is a very strong academic paper prepared by a group including Professor Ian Ramsay and Professor Helen Anderson called the Phoenix Research Team. This research is discussed further below in section 32 of this White Paper.

The report also points out, troublingly for regulators, that there is legal phoenix activity and illegal phoenix activity. They describe legal phoenix activity as business rescue. The key finding of the report is that the difference between types of phoenix activity, i.e. the types that are illegal and types that are legal, comes down to the intention of the company directors. They found:

The behaviour becomes illegal where the intention of the company’s controllers is to use the company’s failure as a device to avoid paying Oldco’s creditors that which they otherwise would have received had the company’s assets been properly dealt with.

More recently, reforms introduced in February 2020 within the Treasury Laws Amendment (Combating Illegal Phoenixing) Act 2019 (Cth) have helped provide a greater understanding of what illegal phoenix activity entails. The key reform was the introduction of creditor-defeating dispositions. A creditor-defeating disposition occurs when a company transfers property for less than its reasonable market value. The implementation of creditor-defeating dispositions into Australian law has helped define phoenix activity and provides a new mechanism that liquidators can use to claim assets.

Despite this reform, it is still safe to say that the definition of phoenix activity is a contested area for regulators, lawyers and academics.

Why is ASIC, ATO and Department of Employment becoming more active in pursuing phoenix activity?

The principal actor that investigates pre-insolvency transactions undertaken by company directors is the liquidator of the company. At law the ASIC has jurisdiction to regulate corporate activity in Australia including laws to protect creditors of companies and powers to undertake independent legal actions against company directors for breach of their duties. If there is a crime committed the matter can be referred to state or federal prosecutors.

The Australian Taxation Office (ATO) and the Department of Employment, Skills, Small and Family Business are both indirectly affected by corporate misfeasance and phoenix activity. The ATO is affected due to its role as collector of taxes and the Department of Employment, Skills, Small and Family Business is adversely affected through payments under the Fair Entitlements Guarantee (FEG). Both have a vested interest in becoming more active in corporate insolvency although they have no direct jurisdiction or powers.

The ATO collects debts payable by companies including PAYG, income tax and GST. Although there is sparse empirical research on the topic, the ATO is usually a substantial creditor in SME liquidations in Australia. FEG is a scheme that pays employees of companies that go into liquidation unpaid employment entitlements that should have been paid by the company in liquidation.

To assist liquidators with claims against directors, both the ATO and FEG may provide funding to liquidators.

In 2016 the Minister for Employment announced that they had provided funding to the special purpose liquidator of Queensland Nickel to undertake proceedings for insolvent trading and breach of directors’ duties against Mr Mensik (appointed director) and Mr Palmer (alleged shadow director). FEG paid an amount of approximately $66.8 million to 759 ex-employees of Queensland Nickel. The minister stated that this action should:

send a very clear message to the defendants that it will take all steps it can to ensure that they face court.

The ATO and FEG are increasing their involvement in liquidations and supporting liquidators in taking action against directors. It is likely that the ATO will attend a creditor’s meeting and that the ATO and/or FEG may potentially fund a liquidator to take legal action against the directors.

Beyond this, the new creditor-defeating disposition reforms have bolstered ASIC’s ability to combat illegal pheonixing activity and protect legitimate creditors by enforcing the creditor-defeating disposition provisions. ASIC now has the ability under s 588FGAA to make an administrative order at the request of a liquidator or on its own initiative stating that the property involved in a creditor-defeating disposition be returned, that the amount representing the benefit be paid or that an amount that ‘fairly represents’ the proceeds be paid. Any failure to comply with the order, is an offence which carries a fine of up to 30 penalty units or imprisonment of up to six months, or both. This extends the recovery provisions available to liquidators and improves their ability to recover assets lost through illegal phoenixing. The benefit is also that liquidators don’t need to start litigation to recover property.

What is the difference between a secured and unsecured creditor?

In corporate insolvency, a creditor is broadly anyone that has a debt or claim. [5] The types of claims creditors can have include basic debts and claims for damages, as well as contingent claims that haven’t given rise to a loss yet but may in the future.

An unsecured creditor is a creditor that has no security over collateral that they can call upon. This means that they have no “cover” and if a company goes into liquidation they need to wait for a dividend from the liquidator to see any return. If their debtor goes into voluntary administration, then their debt may be compromised by a deed of company arrangement that is voted on by creditors.

A security interest is a right that a secured creditor takes over collateral (i.e. the property) in return for providing a loan or other advance of value. For example, a bank will take a security interest over a property when it loans a company money to buy that property.

There are two types of security interest:

- Non-circulating security interests (such as land, plants and equipment)

- Circulating security interests (such as cash, stock and debts owed to the company)

A security interest may also refer to a charge over property, and it is the bundle of rights that a secured creditor has.

In Australia an unsecured creditor in a liquidation or voluntary administration faces dim prospects of recovery of any substantial amount. The difference between an unsecured and a secured creditor is that a secured creditor has collateral that they may call upon if their debtor goes into insolvency.

Insolvency issues for SMEs

What are SMEs and why are they important?

A small-to-medium size enterprise (SME) is any business that employs up to 200 employees. The Australian Bureau of Statistics (ABS) reported in its count of Australian businesses that in June 2018 there were more than 2.3 million actively trading businesses in Australia and of these:

- 542, 685 businesses had 1-4 employees (microbusinesses);

- 187, 360 businesses employed 5-19 employees (small businesses); and

- 49, 202 employed 20-199 employees (medium businesses). [6]

The smaller size of SMEs, compared to large corporations and government entities, belies the importance of this segment to the economy. SMEs accounted for 34% of Industry Value Added and 29% of all wages and salaries paid in selected industries of the private sector in 2017-18. [7]

The ABS also reported that in 2017-18, businesses with a turnover from $50k to less than $200k had the highest entry rate (20.6%) and businesses with less than $50k had the highest exit rate (19.4%). [8] Although “exit” does not necessarily mean all those businesses had become insolvent we can still assume that a significant proportion were insolvent or at least unviable.

97.4 percent of micro businesses are wholly Australian owned, [9] and they are more reliant upon a smaller number of customers that are members of their local community. This means that SMEs are going to be closer to their local communities and that facilitating the prosperity of SMEs will have a positive impact on local communities throughout Australia.

Small-to-medium sized businesses are therefore the backbone of the economy and local communities.

What financial and operational issues do SMEs face?

The two main root causes of insolvency issues that are faced by SMEs today are:

- Australia’s slow paying culture by customers; and

- Poor management of SMEs.

Other issues that SMEs face that cause insolvency include:

- Poor access to finance;

- Implementing big projects that aren’t properly financed or provisioned for;

- Growing too fast (overtrading);

- Timing; and

- Combining one of the above causes with a predictable risk event occurring and creative accounting.

Cause 1: Australia’s poor payment culture

Australia has a culture of slow payers in business and this is exacerbated in some industries such as building and construction.

A discussion paper released by the Federal Government regarding the ‘Prompt Payment Protocol’ asserted that 90% of small business failure is caused by poor cash flow. [10] In plain English, that means that the customers/clients of SMEs trigger insolvency by not paying their bills on time. The paper uses empirical research to show that Australia has a national culture of paying suppliers slowly in the business-to-business (B2B) context. The research compares Australia and New Zealand’s B2B debt payments and found that there is a marked difference between the times it took for these debts to be paid. The results for B2B debt payments from the date an invoice was issued were:

Australia 54.1 days v NZ 43.1 days. [11]

This is not so much a legal issue but a micro-economic reform issue because SMEs are particularly vulnerable to cash flow crunches. The best example is the building and construction industry which has historically had both the highest proportion and number of insolvencies compared to other industries. To remedy this, construction contracts with “pay when paid” terms for payment were outlawed and subcontractor payments sped up through the Security of Payment legislation. [12]

Often the question is asked, ‘what is the point of no return in the spiral to insolvency?’ The answer is that there are several key indicators, including:

- Chronic insolvency

- Winding up applications

- Director Penalty Notices from the ATO

- Staff walking out the door

- Being put on stop by suppliers

- Deadlock between owners and/or management about the future of the business.

While these are all signs of a spiral towards insolvency, it is important to note that these are symptoms rather than root causes of insolvency. These symptoms will follow the causes and trying to cure the symptom will ultimately lead to frustration.

If we think like doctors about causes and symptoms, the research supports the proposition that poor management, the big project and overtrading are the most common root causes of insolvency.

Cause 2: Poor management

The bad news is that the prime cause of business failure is poor management. One definition of management is the art of “getting things done through others”. [13] Another definition by Peter Drucker defines management as a “multi-purpose organ that manages business and manages managers and manages workers and work”. The first hint from those definitions is that good management understands they don’t have the job of doing everything in a business.

There is no simple way to learn to manage a business because it is an art that is learnt through practice and experience.

Here is what to look out for as indicators of poor management:

- Refusal to seek or take advice: A director should look to advisors who have been through insolvency situations and understand the strategic issues that the business faces;

- Narrow-mindedness: Directors who only show interest in matters that concern their particular area of expertise or interest. Also directors that lack financial experience and/or do not have suitable financial advisory services at hand; and

- People skills: There is no need to have a business study accreditation or a great deal of emotional intelligence to establish high-level performance expectations. Down-to-earth, direct and goal-oriented managers are likely to get the most from their staff.

Australia has recognised that it needs to encourage entrepreneurs to move past business failure. In 2016 the Federal Government announced a plan to improve the “balance” of insolvency laws to encourage entrepreneurs. This was implemented within the Insolvency Law Reform Act 2016. According to the Australian Financial Security Authority, the amendments aim to:

- remove unnecessary costs and increase efficiency in insolvency administrations;

- align the registration and disciplinary frameworks that apply to registered liquidators and registered trustees;

- align a range of specific rules relating to the handling of personal bankruptcies and corporate external administrations;

- enhance communication and transparency between stakeholders;

- promote market competition on price and quality;

- improve the powers available to the corporate regulator to regulate the corporate insolvency market and the ability for both regulators to communicate in relation to insolvency practitioners operating in both the personal and corporate insolvency markets; and

- improve overall confidence in the professionalism and competence of insolvency practitioners. [14]

The good news for SME directors is that the direction of policy in Australia is to help them to learn from their experiences and continue to innovate and develop businesses after a business failure.

One area that has not been researched is whether sickness is a significant contributor to business failure in SMEs. We are almost guaranteed to be very sick at some time in our lives and a mental or physical illness will impede a director’s ability to properly manage a business. In Australia there is no established ‘locum’ system for SME directors that can provide a person who can easily step into the shoes of a director whilst they are unwell. If directors are sick they may need to look to friends, family or employees to take over a business.

Cause 3: Poor access to finance

SMEs have historically suffered from higher costs of capital and after the Global Financial Crisis (GFC) the problem was exacerbated. Before the GFC (2001 to 2008) SMEs paid a premium of at least 1.5% above the interest rates paid by large businesses but since that time the spread has jumped to at least 2%. [15] SMEs are reported to most commonly seek finance to maintain short term cash flow or liquidity. [16]

Access to finance is a critical issue faced by SMEs and anecdotal evidence suggests that the banks are avoiding lending to SMEs overall.

Cause 4: The Big Project

Entrepreneurs are likely to be optimistic. They may take on a big project without up-to-date financial information or reasonable forecasts. Costs and timeframes are often underestimated and/or revenue is overestimated and this may lead to insufficient working capital.

The risky ‘big project’ could include any one of the following:

- Taking on a larger than usual contract

- Building a side business

- Creating a new product line

- Implementing a new software system

- Outsourcing or offshoring a key function of the business

- Acquiring another business

Cause 5: Overtrading

It is obvious to point out that business growth costs money (i.e. working capital) because additional funds are required to build a business before actual income from increasing revenue is received. Overtrading is engaging in more business than can be supported by the funds or resources available to the directors.

Overtrading is another major cause of business failure. A director may set a sales target for the business that is reached but they also need to consider the working capital required to fund this growth.

If a business overtrades it may need to seek additional funds from a line of credit or a director’s loan.

One form of overtrading is offering ‘easy’ credit to customers by way of taking on poor quality clients or granting them extended trading terms. Both of these options for building business need to be carefully considered before being undertaken.

Cause 6: Timing

Watch out for tax debt enforcement as the final straw before collapse.

The Director Penalty Notice (DPN) regime is a big challenge that is adversely affecting entrepreneurs and directors of SMEs. The ATO is training their staff and automating their processes to issue DPNs regularly. A DPN allows the ATO to pierce the corporate veil meaning that directors may be personally liable for tax debts resulting from unpaid Superannuation Guarantee Charges (SGC) and unpaid PAYG contributions.

Since 2012, directors of SMEs have been held to be personally liable for PAYG and SGC contribution liabilities that are unpaid and unreported for three months. The personal liability accrues irrespective of whether the ATO issues a DPN. However, the DPN now crystallises the date that the personal liability is due to be paid. Personal liability cannot be avoided if the unpaid liability was unreported for three months. Directors will also be unable to avoid personal liability under the director penalty notice by placing the company into voluntary administration or having it wound up.

Once the ATO commences action by way of a DPN or winding up application then the prospects of a company surviving are poor.

Cause 7: Add a predictable business risk event

If a business is already in a tight financial situation because it is overtrading, taking on a big projects, or is otherwise poorly managed, the occurrence of a predictable event may cause the business to fail.

Predictable risk events are not likely to cause a healthy business to fail but they may cause a vulnerable business to tip over. An example of this is an e-commerce website being hacked. Anyone that operates an e-commerce business will be conscious that they may be hacked one day and they may take steps to minimise that risk or even take out insurance.

Unfortunately, there is no way to prevent these normal business risks. Losing a big customer, having a key person in the business resign, an economic downturn or an act of god (e.g. weather), are other examples of predictable risk events.

The established rule of thumb is that a business should have cash at bank equal to at least 3 months of business expenses in order to be covered in the event of a predictable business risk event occurring.

Cause 8: Add creative accounting

When a business is failing it can be tempting to get ‘creative’ with accounting. This is one symptom of impending business failure. Creative accounting can often be an unintended result of trying to ‘reframe’ the problem faced by a business.

Beware if any of the following symptoms occur:

- Delay in producing financial statements;

- Continued payment of dividends (i.e. drawings) by relying on debt rather than retained earnings;

- Cutting expenditure on routine maintenance;

- Starting to treat extraordinary income as ordinary income and vice versa;

- Changing the ownership title of main assets in the business;

- Valuing assets at inflated figures;

- Meeting company debts out of the director’s own pockets; and

- Valuing stock of dated products at the current market selling price rather than at cost.

What is the legal meaning of insolvency?

Insolvency is an important concept for directors because it is a long established legal rule that when a company approaches insolvency they are under a duty to consider the interests of creditors.

Section 95A of the Corporations Act 2001 (Cth) (the Act) defines “insolvency”. Under the Act, a company is insolvent if it is unable to pay its debts as and when they become due and payable. It is known as a “cash-flow test” of insolvency, because a company may have more assets than liabilities on their balance sheet but are considered to be insolvent because they cannot realise their assets fast enough to satisfy their debts as they become due and payable. To be insolvent, a company must have an endemic shortage of working capital rather than be suffering from a temporary lack of available cash.

The “cash-flow test” is preferred over other tests of solvency because it is a more accurate test of the viability of a company’s business. A company with substantial debts may be able to trade its way out of difficulties if the debts are long term and the company is profitable.

The “cash-flow test” requires an analysis of:

- The company’s existing debts;

- Whether the company’s debts are payable in the near future;

- The date each debt will be due for payment;

- The company’s present and expected cash resources; and

- The dates any company income will be received.

A Court analysing solvency will consider whether the company is suffering from a temporary lack of liquidity (and therefore is not insolvent) or whether the company faces an “endemic shortage of working capital”. In order to find that a company is insolvent, a Court will need to be convinced that the company has gone past the “point of no return” and that it is no longer viable to trade.

A Court is also able to find that a company is presumed to be insolvent due to its failure to keep books and records as required by section 286 of the Corporations Act. In order for this presumption to be made, a liquidator needs to prove that either no records at all were kept or that the records that were kept are factually inaccurate and do not allow an accurate picture of the company’s affairs to be reconstructed. [17]

What are the indicators of insolvency recognised by Courts?

Insolvency is usually worked out retrospectively in Court, so what is more useful to directors is to understand the forward indicators of insolvency. Unfortunately, this isn’t an exact science but there are a number of indicators that will be looked at adversely by the Court and creditors.

In ASIC v Plymin & Ors (2003) 46 ASCR 126 (commonly referred to as the “Water Wheel case”), Justice Mandy of the Supreme Court of Victoria referred to a checklist of 14 indicators of insolvency:

- Continuing losses;

- Liquidity ratio below 1 (a ratio of current assets to liabilities);

- Overdue Commonwealth and State taxes;

- Poor relationship with present bank including inability to borrow additional funds;

- No access to alternative finance;

- Inability to raise further equity capital;

- Supplier placing the debtor on COD (Cash on Delivery) terms, otherwise demanding special payments before resuming supply;

- Creditors unpaid outside trading terms;

- Issuing of post-dated cheques;

- Dishonoured cheques;

- Special arrangements with selected creditors;

- Solicitors’ letter, summons(es), judgments or warrants issued against the company;

- Payments to creditors of rounded figures, which are irreconcilable to specific invoices;

- Inability to produce timely and accurate financial information to display the company’s trading performance and financial position, and make reliable forecasts.

It is possible for a company to remain solvent even when many of the above factors are present. This is particularly true where sufficient outside funds are available, such as funds from a director, a new financier or an incoming investor.

Directors and advisers of SMS

What are the principal legal duties of directors?

Being a company director means that you assume personal legal duties. These duties cannot be delegated and the law is designed to limit the excuses for breach that directors have to avoid sanctions or paying compensation. In an insolvency scenario, a liquidator may look to enforce these claims (on behalf of the company and creditors) against the former directors.

The duties of company directors include both common law and statutory duties. These duties are set out below.

Common law (or fiduciary) duties:

Duty to act in good faith

Directors have a duty to act in good faith in the interests of the company as a whole. The test as to whether this duty has been complied with is a subjective test of “honesty or good faith”.

Directors are in breach of this duty where they fail to give proper consideration to the company’s interests. When considering the interests of the company, a director must take into account the interests of shareholders and creditors (in the case of an insolvent company).

Duty to exercise powers for a proper purpose

Directors must not use their powers for an improper purpose. The test of whether a director has used their powers for an improper purpose is an objective test. Improper purposes may include when a director uses their power to gain an advantage for themselves, [18] or by manipulating voting power.

Regardless of whether the improper purpose is the dominant cause or one of a number of contributing causes to a director’s decision, the act will be invalid if, but for the improper purpose, the decision would not have been made. [19] This is eloquently called the ‘but for’ test.

Duty to retain discretion

Directors must not put themselves in a position where they are unable to act in the best interests of the company. For example, a director cannot contract with a third party to vote in a certain direction at board meetings.

Duty to avoid conflicts of interest

Directors must not put themselves in situations where their personal interests conflict with the interests of the company. If a director’s duty to avoid conflicts is breached the director becomes liable to the company for any benefit derived, or to indemnify the company’s loss. In addition, the company may void any contract that a director enters or has entered into as a result of the conflict of interest.

Statutory duties under the Act

Section 180(1) – Duty to act with care and diligence

Section 180 (1) reinforces the common law duty of the same name. Section 180(1) requires an objective standard of care, stipulating that a director or other officer of a corporation must exercise their powers and discharge their duties with the degree of care and diligence that a reasonable person would exercise if they:

- were a director or officer of a corporation in the corporation’s circumstances; and

- occupied the office held by, and had the same responsibilities within the corporation as a director or officer. [20]

Additionally, a director will be considered to have acted with the due care and diligence required when they have complied with the “business judgment rule” in making decisions relevant to the business of the company. The business judgment rule provides that a director must:

- make the judgment in good faith or for a proper purpose; and

- not have a material personal interest in the subject matter of the judgment; and

- inform themselves about the subject matter of the judgment to the extent they reasonably believe to be appropriate; and

- rationally believe that the judgment is in the best interests of the corporation. [21]

Section 181(1) – Duty to act in good faith

This duty is consistent with the equivalent common law duty. Section 181(1) requires a director or other officer of a corporation to exercise their powers and discharge their duties:

- in good faith in the best interests of the corporation; and

- for a proper purpose. [22]

Section 182 – Duty not to make improper use of position

This section provides that a director must not improperly use their position to gain an advantage for themselves or someone else, or to cause a detriment to the corporation. [23]

This duty is breached if a director has the intention and purpose of obtaining an advantage or causing a detriment, regardless of whether an actual benefit or detriment occurs in fact. [24]

Section 183 – Duty not to make improper use of information

This section provides that a person who obtains information because they are, or have been, a director of a corporation must not improperly use the information to:

- gain an advantage for themselves or someone else; or

- cause detriment to the corporation. [25]

This duty continues after the person stops being an officer or employee of the corporation.

Section 588G – Duty not to trade whilst insolvent

This section provides that directors must ensure that the company does not incur a debt while insolvent. A person breaches this duty where:

- he or she is a director of the company when it incurs a debt;

- the company is insolvent at the time, or becomes insolvent by incurring the debt;

- at that time, there are reasonable grounds for suspecting that the company is insolvent, or would become insolvent by incurring the debt; and;

- he or she failed to prevent the company from incurring the debt. [26]

A director may also face criminal penalties for breaching this duty if his or her failure to prevent the debt was dishonest. [27]

Section 191 – Disclosure of material personal interests

This section provides that a director of a company who has a material personal interest in a matter that relates to the affairs of the company must give the other directors notice of their interest. [28]

There are various exceptions to this rule, including section 191(5), where companies with only one director are excluded.

Section 286 – Financial records

This section provides that a company must keep written financial records. This requirement relates to a director’s duty of care and diligence and provides that directors may be subject to a penalty for failing to maintain proper financial records.

Section 588GAB– Officer’s duty to prevent creditor-defeating dispositions

An officer of a company must not engage in conduct that results in the company making a creditordefeating disposition of property of the company.

What is insolvent trading?

Directors are under a duty to prevent insolvent trading under section 588G of the Corporations Act. A claim under section 588G is only available to a liquidator after a company has been placed into liquidation.

For a liquidator to make a claim for insolvent trading against a director or former director the following elements must be satisfied:

- the person was a director at the time that the debt was incurred;

- the company was insolvent at that time, or became insolvent by incurring the debt;

- at the time, there were reasonable grounds for suspecting insolvency, or that the company would become insolvent by incurring the debt; and

- at the time, the director was aware that there might be grounds for suspecting insolvency or that a reasonable person in their position would be so aware.

If the director suspects that the company was insolvent at the time the debt was incurred and their failure to prevent the debt was dishonest, they are also liable for criminal punishment.

Liquidators have a period of 6 years after their appointment to commence a claim against a director for insolvent trading. After that date passes the commencement of a claim is statute barred.

If the liquidators choose not to pursue a claim for insolvent trading, the company’s creditors (individually or in a group) may commence their own actions against the directors for insolvent trading, but this is limited to the debts owed to the creditors. Creditors may make a claim at any time if they have consent from the liquidator but they may only request the liquidator’s consent after the liquidator has been appointed for 6 months. It is rare that a liquidator would make an insolvent trading claim because they would need to prove the insolvency of the company and this is not a simple task.

The duty to prevent insolvent trading does not apply when a director is able to claim protection under the new safe harbour from insolvent trading (section 588GA of the Corporations Act).

How does a director get a safe harbour protection from insolvent trading?

The new safe harbour from insolvent trading is the most significant reform in corporate insolvency since the introduction of voluntary administration in 1993. The new reform can be used in conjunction with, or implemented separately to, a pre-pack insolvency arrangement.

In September 2017 the Federal Government passed the Treasury Laws Amendment (2017 Enterprise Incentives No 2) Bill 2017 which inserted a new section 588GA into the Corporations Act 2001 (Cth). The amendment gives directors the right to enter a “safe harbour” protecting them from personal liability for trading their company whilst it is insolvent.

The prohibition on insolvent trading is a very strong disincentive for directors from attempting an informal restructure or work-out because they are at risk of personal liability for trading whilst insolvent.

Requirements for safe harbour protection

Entry into the safe harbour doesn’t occur automatically. Directors must comply with the requirements of the Act and will only have protection from personal liability for insolvent trading if:

- At the time they suspected or knew the company was insolvent they start developing a course of action that at the time of development was reasonably likely to lead to a better outcome for the company than proceeding to immediate administration or liquidation; and

- The debt was incurred directly or indirectly in connection with a course of action.

Companies are also required to pay all staff entitlements during this period and comply with tax reporting obligations, or they will lose the protection of the safe harbour for all debts that were incurred.

Course of action reasonably likely to lead to a better outcome

Determining whether a course of action is “reasonably likely” to lead to a better outcome will vary on a case by case basis. A course of action in this context refers to a turnaround or restructuring plan that has the objective of putting the company in a better position than it would be in a voluntary administration or liquidation scenario.

In the explanatory memorandum for the new legislation, the required standard of “reasonably likely” is a chance of achieving a better outcome that is not fanciful or remote, but is “fair”, “sufficient” or “worth noting”.

Section 588GA(2) outlines a non-exhaustive list of factors that are taken into account when determining whether a course of action taken by a person was reasonably likely to lead to a better outcome. These include the directors:

- Keeping themselves updated with the financial position of the company;

- Taking appropriate measures to prevent officers or employees from hindering the ability of the company to pay its debts;

- Taking appropriate measures to ensure financial records are kept;

- Obtaining advice from an “appropriately qualified entity”; and

- Implementing the restructuring plan to improve the company’s financial position.

Best practice

In light of the requirements of section 588GA, the Turnaround Management Association (TMA) has published best practice guidelines to guide the safe harbour process. The flow chart of best practice can be obtained on the TMA website.

Key stages of the TMA best practice include:

- The safe harbour period will begin at the time a person starts developing a course of action, of which will include an initial financial assessment of the company when the directors suspect the company may be insolvent.

- After it is determined that the company is insolvent, the directors should engage an “appropriately qualified entity” to assess the availability of entry into the safe harbour. If they receive advice that they should enter the safe harbour, the directors should then begin to develop a turnaround or restructuring plan.

- Once the plan is developed it must be put into action. If it is not actioned within a reasonable period of time (of which is determined by the complexity of the restructure) directors will lose the benefit of the safe harbour.

- The turnaround or restructuring plan must be continually monitored so that the success or failure of the plan can be measured. It may be the case that the plan hasn’t worked as intended and steps need to be taken to place the company into administration or liquidation.

Challenges for SMEs

Crucially, each stage of the process should be carefully documented so that directors can prove they have met their threshold obligations. It is this evidentiary burden that may provide a challenge for SMEs who may not have sufficient professional support to document their claim for safe harbour protection.

Why do directors need to watch out for Director Penalty Notices (DPNs) from the ATO?

The DPN regime is a targeted instrument used by the ATO to pierce the corporate veil and make directors personally liable for company tax debts. The key mistake made by directors is non-compliance with lodgement obligations. That means if directors don’t lodge their tax returns on time, they could be liable for a DPN.

A director of a company is under an obligation to ensure that their company remits all withheld Superannuation Guarantee Charge (SGC) and PAYG amounts to the ATO. A director can be held personally liable for a penalty equal to the amount of the company’s unpaid PAYG and SGC debts, upon failing to ensure these debts are remitted when due.

To recover a penalty from a director, the Commissioner will issue a DPN and must wait until the 22nd day after issuing the notice before commencing proceedings (the timeframe for compliance with a DPN commences on the date on which it is posted).

If a director is issued with a DPN there are limited options available to have the penalty remitted, however in order for the penalty to be remitted, action must be taken within 21 days of the notice being issued. For unpaid amounts that were reported in the company’s Business Activity Statements (BAS) or Superannuation Guarantee Statements (SGS) within three months of their due date, the penalty will be discharged upon payment of the debt, or if a voluntary administrator or a liquidator is appointed. If the unpaid amount was not reported within three months of the due date for lodgement, the debt must be repaid by the company to have the director’s personal liability remitted.

This means that the directors of the company are personally responsible for the debt if the company leaves it unpaid.

If no action is taken before the 22nd day after the DPN is issued to the director, the penalty is not remitted and the director is held personally liable for the penalty amount until it is paid in full. To enforce this claim against the directors personally, the ATO will then issue court proceedings for a liquidated claim in the amount of the outstanding debt.

New directors are not immune from the personal liabilities incurred by a DPN but a new director will not become liable for any existing PAYG or SCG debt until they have served as a director for 30 days. If the director remains a director of the company after the 30 day period has elapsed, they are then also personally liable for any outstanding PAYG and SGC debts. New directors however, will not be subject to the restricted remission options until 3 months after they become director of the company, regardless of how long the company has been liable for the debt.

The liability for a DPN is subject to very limited defences that are unlikely to be utilised in most cases.

What penalties can directors face for insolvent trading and breach of duty?

Directors can face a number of consequences for insolvent trading and breach of their duties. The penalties include civil penalties, compensation proceedings and criminal charges.

All company directors have a duty under section 588G of the Act to prevent insolvent trading. A director of a corporation must also exercise their powers and discharge their duties with a certain degree of care and diligence as stipulated by sections 180-184 of the Corporations Act. A breach of either of these fundamental responsibilities by a director can lead to significant consequences for the directors personally, and the company as a whole.

Penalties include:

- On application for a civil penalty order, the court may order compensation; [29]

- If a court finds a person guilty of an offence under s 588G(3) in relation to a company incurring a debt whilst insolvent, the criminal court may order compensation; [30]

- A creditor may sue for compensation; [31] and

- A director may be held liable to indemnify the Commissioner of Taxation for unpaid debts. [32]

Criminal penalties

Section 184(1) of the Actprovides that:

“(1) a director or other officer of a corporation commits an offence if they:

- are reckless; or

- are intentionally dishonest;

and fail to exercise their powers and discharge their duties:

- in good faith and in the best interests of the corporation; or

- for a proper purpose.

Schedule 3 of the Act provides that for a breach of section 184 above, directors may face fines of up to $360,000 or 5 years imprisonment, or both.”

Section 206B of the Act provides for the automatic disqualification of directors from managing corporations if they are convicted of a criminal offence related to the company.

Civil penalties

The ASIC is responsible for the Australian securities regulation and has the power to apply for a declaration of contravention, a pecuniary penalty order and/or a compensation order under section 1317J of the Act. A creditor may also sue a company under the Act, for compensation. The Court may also order, on application by the ASIC, to disqualify a director from managing corporations. [33]

Under division 4 of the Act, a director is liable to compensate the company for loss resulting from insolvent trading. [34] The director may face one of a number of consequences for any loss occurring to the company as a result of insolvent trading:

- The court may order the director to compensate the company for an amount equal to the loss or damage caused by the breach. [35]

- A creditor may recover from the director an amount equal to the loss or damage caused by the breach. [36]

- If the breach is proven to be a result of the director’s dishonesty, the director may be found guilty of a criminal offence, punishable by a fine or imprisonment. [37]

The new creditor-defeating disposition reforms introduce criminal and civil penalties for individuals and corporate bodies that contravene the duties outlined above. To be held criminally liable the individual or body must have been reckless as to the result of their conduct and to be held civilly liable the individual or body must have been unreasonable in their conduct. If such a standard is proven, hefty penalties can be enforced by the court including fines of up to 4 500 penalty units for individuals and 45 000 penalty units for corporations. Individuals can also be imprisoned for up to 10 years and corporations can be fined up to 10% of their annual turnover.

What immediate actions should directors of an SME take if their company is insolvent?

If a business is insolvent and it is unable to pay its debts when they fall due and payable, there are a number of risks that directors need to be prepared for. The first issue to consider is whether the insolvency is temporary, or whether there is an endemic shortage of working capital.

If there is an endemic shortage of working capital, the director’s first steps should be:

- Seek or advance further working capital (debt or equity);

- Take steps to improve the quality of real time financial information for decision-making; and

- Talk to professional advisors to develop a game plan (exit or business continuity).

Seek or advance more working capital

Given there is an endemic shortage of working capital, cash is king! The first step may be to seek or advance further working capital for the business, however, in the long term, this does not solve the problem if the business has a loss making business model.

Immediate options are:

- Receivables finance: Many businesses as a first step look at unlocking debtors by utilising receivables finance (also known as invoice discounting). This has the benefit of providing immediate access to funds waiting to be paid by debtors.

- Friends, fools and family: You can seek working capital (either debt or by granting equity) from those close to you. However, it is unlikely that there will be an alignment of interests and your lenders are unlikely to be able to assess the risks of lending to you. This may put pressure on your relationships in the event of non-payment and permanently damage relationships.

- Trade suppliers: You can contact your trade suppliers and ask them to extend terms. This will have the same effect as a bank overdraft extension on your financial position.

If directors advance money themselves they should consider whether they can obtain a security interest over business assets. If directors advance monies out of their own pocket without security they will become unsecured creditors in the event of company failure unless they obtain a security interest.

Obtain reliable financial information

Reliable financial information will help prevent a business from choosing the wrong strategy by giving the directors insight into why the business isn’t achieving the required rate of return. There are three simple ways to ensure a business has reliable financial information:

- Draw up an annual budget and cash flow forecast, and as the year goes on compare the budget cash flow with actual figures;

- Ensure you know what your product/service costs to produce and what affect it would have on profits if for example, sales were increased or decreased by 10%; and

- Make sure your assets are valued correctly.

When a business is failing it can be tempting to get ‘creative’ with accounting and this is one symptom of impending business failure. Avoid the temptation to:

- Delay producing financial statements;

- Continue paying dividends (i.e. drawings) through incurring debt rather than retained earnings;

- Cut expenditure on routine maintenance;

- Start treating extraordinary income as ordinary income and vice versa;

- Change the ownership title of main assets of the business;

Value assets at inflated figures;

- Meet company debts out of your own pocket; and

- Value stock of finished products at the current market selling price rather than at cost.

What is your end game? Business continuity or business exit?

When a business hits rocky times the directors need to develop a clear business strategy. If the directors do not have a clear strategy they may get lost in the details of keeping the business afloat rather than driving towards their end game. If there is a profitable core that is worth saving, there is a choice between keeping the business and attempting to salvage it or selling the business.

A pre-pack insolvency arrangement is an alternative to appointing a voluntary administrator to salvage business value. The pre-pack insolvency arrangement gives the director the opportunity to consider a more orderly approach to a restructure before any formal appointment.

What types of professional advisors assist with a pre-pack insolvency arrangement?

The worst case scenario would be for a director of an insolvent SME to engage a group of different advisers without having one particular co-ordinating adviser. A consensus model for professional advisers would be sure to fail in a turnaround scenario.

It is likely that a lawyer, financial accountant and insolvency practitioner with different briefs will pull in opposite directions. Each professional will have a different methodology, timeframe, priorities and task list.

There are a number of different advisors who market themselves as being capable of providing advice, and helping with the setup, and/or supervision of, pre-pack insolvency arrangements. These are:

- Small firm accountants

- Insolvency practitioners

- Lawyers

- Pre-insolvency advisers

Small Firm Accountants

Most directors will have an existing relationship with an accountant. These accountants are typically based at small suburban accounting practices with 2-3 partners or they are a sole practitioner.

Small firm accountants provide advice regarding:

- Business growth and working capital;

- Estate planning and superannuation;

- Business and personal taxation; and

- Audit compliance.

- Small firm accountants are usually members of either CPA Australia or Chartered Accountants, however it is not a legal requirement for a practicing accountant to be a member of either professional body. While these professional bodies do have entry requirements, neither organisation requires its members to have deep insolvency knowledge.

Small firm accountants are unlikely to have thorough insolvency training and their knowledge is often obtained from attending creditors meetings, reading liquidation and administration reports and talking to clients about their business failures. Deep knowledge of insolvency would require both a detailed understanding of the Corporations Act and policy regarding the insolvency regime and training in strategy from insolvency practitioners.

Accountants usually charge fees at an hourly rate broken down into 6 minute units. Small firm accountants are not usually paid per deliverable and their charging is opaque to an end client because the client has no understanding about the steps required to complete the task they engage their accountant to complete.

It is also unlikely that general accountants work specifically or regularly in the area of insolvency. While a small firm accountant can provide advice on certain aspects of a pre-pack insolvency arrangement, such as the taxation implications of transactions, they are unlikely to be ready to supervise or set-up a pre-pack insolvency arrangement because they do not have the specialist insolvency knowledge necessary.

Another issue with a small practice accountant is time. They are likely to have over 100 ongoing clients and will need to juggle their other clients with a turnaround client. It is unlikely that they will have the time to “drop everything” and work on a turnaround.

Insolvency Practitioner

Insolvency practitioners are individuals registered with ASIC as liquidators. The peak body in Australia that represents insolvency practitioners is the Australian Restructuring, Insolvency and Turnaround Association (ARITA). However, it is not essential that registered liquidators be members of ARITA.

Insolvency practitioners are qualified to provide advice, and assist in the set-up, or supervision of a pre-pack insolvency arrangement. Insolvency practitioners are likely to have a thorough and up-to-date understanding of insolvency law and practice that they have developed through education and day-to-day work on company liquidations and voluntary administrations.

Insolvency practitioners generally charge an hourly rate, broken down into 6 minute units. Different staff members working below them then charge at different rates based on experience in formal appointments. The limit on fees charged by insolvency practitioners is usually the value of the assets of the company in liquidation or administration, however there may also be creditor or director funding beyond this. In formal appointments, the fees charged need to be approved by creditors, but if they fail to obtain this approval from creditors, the insolvency practitioner can apply to a Court for approval. Insolvency practitioners will usually discuss options that directors have before taking an appointment as liquidator or voluntary administrator and often they do not charge for this advice because they generally expect to recover their fees once they are appointed.

Insolvency practitioners are subject to rules which limit their capacity to provide advice, help with the setup, or supervise a pre-pack insolvency arrangement. When they are approached, insolvency practitioners are required to turn down a formal appointment if they have a conflict of interest. The ARITA Code of Professional Practice for insolvency practitioners states that an insolvency practitioner must refuse an appointment where the practitioner has provided non-general advice to one of the directors of the insolvent company in respect of the director’s duties to the insolvent company. [38] Insolvency practitioners are also required to refuse appointments where they have had a professional relationship with the insolvent company within the previous two years. [39] As a result of these conflict rules, insolvency practitioners are disqualified from setting up and supervising a pre-pack arrangement if they intend to be later appointed as voluntary administrator or liquidator. The rationale for this limitation is that giving any kind of specific advice regarding a pre-pack insolvency arrangement may undermine an insolvency practitioner’s impartiality.

There is also a larger issue to be considered by a company director about a conflict of interest. If an insolvency practitioner advocates for a pre-pack insolvency arrangement, they may only receive a fraction of the fees that they could have generated from a voluntary administration. Therefore, there is a risk that due to this conflict of interest, insolvency practitioners may steer directors towards voluntary administration rather than a less expensive pre-pack insolvency arrangement.

Lawyers

Specialist insolvency lawyers can advise regarding the legality of a pre-pack insolvency arrangement and supervise the setup of a pre-pack arrangement. Lawyers who specialise in the field will have an up-to-date knowledge of insolvency law, however lawyers are not usually experienced in all aspects of a pre-pack insolvency arrangement. Whilst they are qualified to supervise the pre-pack process and provide advice on its legality, most lawyers are not experienced in the financial and practical aspects of setting up of a pre-pack insolvency arrangement. This is principally because lawyers generally only provide “legal services”.

Specialist insolvency lawyers are generally more expensive, charging rates of around $400-$600 per hour, broken down into 6 minute units. Legal services are defined in section 6 of the Legal Profession Uniform Law as “work done, or business transacted, in the ordinary course of legal practice”. [40] Most tasks in the preparation of a pre-pack arrangement relate to consulting and business strategy and therefore are not strictly “legal services”. Most lawyers will choose not to undertake these tasks, and are likely to want to restrict their involvement to providing services that are within the scope of legal services (i.e. advising on the transactions involved in the pre-pack arrangement and drafting documents).

On the other hand, it may be essential to have a lawyer draft a business sale or asset sale contract. A pre-pack insolvency arrangement may be clawed back if a Court finds it is uncommercial, a sham transaction or a creditor-defeating disposition.

Pre-insolvency Advisors

There are a number of consultants that hold themselves out to be pre-insolvency advisors. They do not offer legal or accounting services and are not qualified insolvency practitioners. Pre-insolvency advisors are often led by a charismatic individual who will have experience in some field of business without necessarily having extensive experience in insolvency. Pre-insolvency advisors are also often employed by financiers and insolvency practitioners for lead generation (i.e. business development on a commission-basis).

Their charging structures vary depending on the advisor, but there is often a sign-up fee involved as well as a fee based on a percentage of the turnover of the company.

Pre-insolvency advisors are not registered with the ASIC. They do not have an overarching body with a code of conduct to which they need to comply, or any necessary level of experience or training benchmarks. This is in contrast to both lawyers and insolvency practitioners who have professional bodies to whom they are answerable to. The key takeaway is that these advisors frequently have inadequate knowledge and experience of insolvency. Due to their inadequate training and lack of insolvency experience, pre-insolvency advisors often have no explainable methodology for company restructuring. At the lowest end of the market these consultant’s stock-in-trade is helping directors to illegally hide assets and engage in phoenix activity.

However, if a pre-insolvency advisor has industry-specific knowledge built up from experience, they may be useful. Directors should test the knowledge and qualifications of pre-insolvency advisers before engaging them to lead a turnaround.